KEY PROJECT RISKS

Project finance is subject to several types of risks. It is useful therefore to look at these risks by category and identify their features and characteristics.

Entity risks

Each project finance participant has a different perspective on risk, often based on the role it is playing in the overall project financing structure. The view of risk moreover is subjective and based not only on economic factors but on characteristics relating to the financial condition of the participant. A particular risk, event or condition that is unacceptable to one party may be considered manageable and routine by another. The identification of risks and knowledge of the participants is therefore essential if a project financing is to be assembled successfully. The risk perspective of each participant in a project financing is presented in the following :

Sponsors. The project sponsors’ objectives are based on the very reasons the project finance exists. Due to the complexity of project financings, the sponsor is interested in several objectives, such as limiting further development costs, minimizing transaction costs, recovering development stage expenses and earning construction, management, or similar fees to fund project company construction activities for the project. And in the long term, the sponsor is motivated with the cash flow generation potential of the project. The sooner the project financing comes on stream, the sooner the sponsor benefits from the revenues generated. Thus, the sponsor would want to mitigate any risks which might delay or prevent the project from coming on stream.

Lenders. The lenders are generally concerned with the economic value of the project, and the legal adequacy of the contracts, and enforceability of the contracts in a loan workout scenario.

Overall, the lender attempts to structure a financing that ensures:

- All costs before construction completion are without recourse to lender for additional funds.

- The contractor satisfies performance guarantees, as evidenced by performance tests.

- There is recourse to other creditworthy project participants for delay and completion costs if the project is abandoned and if minimum performance levels are not achieved.

- There are predictable revenue streams that can be applied to service debt.

- The revenue streams are long term, from a creditworthy source and in an amount that covers operating costs and debt service (off-take agreement).

- The project maximizes revenue while minimizing costs, complying with environmental laws in order to maintain long-term viability.

D&B Contractor. The relationship between the sponsors and D&B (Design & Build) contractor is based on the fact that the turnkey nature of the construction project requires the contractor to deliver the project on spec and on time. This means that the contractor is concerned with the difficulty of predicting events that could adversely impact the parameters of the project and avoiding them. There are certain methods of incentivizing the contractor; for example, increasing the construction price or via a bonus payment in the case of early completion. The contractor is also concerned with the underlying financing documents, including whether the sponsor has arranged sufficient financing to pay the contractor for work performed.

O&M contractor. The relationship between the project sponsors and O&M (Operating & Maintenance) contractor is concerned with the need for price and performance predictability of the project. While the other project participants will want to ensure that the operating costs are fixed or predictable so that debt servicing ability can be analyzed, the O&M contractor, in contrast, wants to limit price risk.

The operator can address this risk by agreeing to operate the project according to a budget approved by the project company. The operator moreover agrees to operate the project within the parameters of the agreed-upon performance levels, and according to laws and industry practice.

Suppliers. Suppliers are concerned with the challenges of providing requisite raw materials for the project and seek in return a fair and stable market price. Project participants on the other hand are concerned with quality and timely delivery of the raw materials with minimum price fluctuations.

Offtaker/purchaser. The offtaker is concerned with firm price and quality, and with minimum uncertainty. The project company, in contrast, wants to increase prices as the market will permit, and to be excused from performance failures (without penalties) for limited periods.

Host government. The project can offer the government short term and long term benefits from the project.

- Short term, the government can use the project for political benefits and for attracting other developers to a country.

- Long term, the successful project should improve economic prosperity and, perhaps, political stability, by providing the needed infrastructure.

It is therefore normal that the host country assumes some of the project risks. This is particularly important for large high-profile projects. For example, implementation agreements, negotiated and executed with the host government, can provide a variety of government assurances with respect to the project risks. The host government might be involved in a project in one or several ways. These include as equity contributor, debt provider, guarantee provider (particularly political risks), supplier of raw materials and other resources, output purchaser and provider of fiscal support (reduced import fees, tax holidays and other incentives).

The host government also has an ongoing role. It can ensure a smooth regulatory climate in future by ensuring permit compliance and through regulatory structures.

Transaction risks

The essence of any project financing is the identification of all key risks associated with the project and the apportionment of those risks among the various parties participating in the project. Without a detailed analysis of these project risks at the outset, the parties do not have a clear understanding of what obligations and liabilities they may be assuming in connection with the project and therefore they are not in a position to consider appropriate risk-mitigation exercises at the relevant time.

Should problems arise when the project is under way, it can result in considerable delays, large expenses and arguments as to who is responsible. As a general rule, a particular risk should be assumed by the party best able to manage and control that risk.

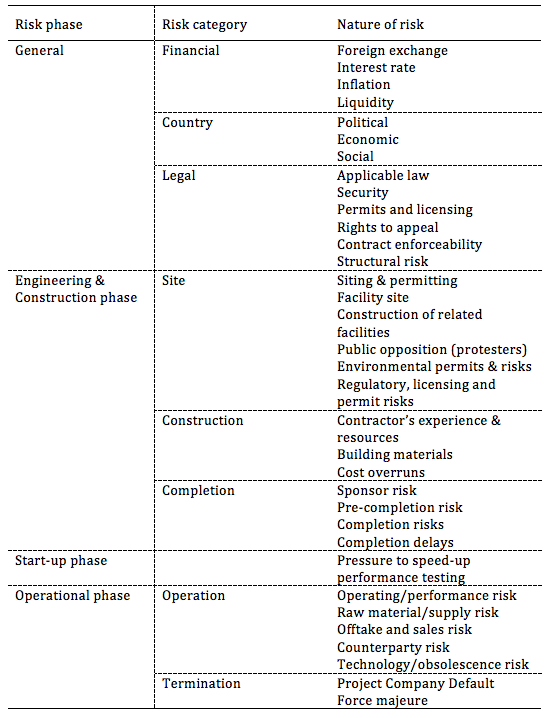

Due to the complexity, each project will have a different risk profile, that is, each project will have different kinds of risks and the magnitude of risks will differ from project to project. In general, however, there are some major areas of risks which should be addressed in every project so that they can be mitigated properly. The following risk matrix sums up the main risks treated below :

Risk matrix in project finance projects

Preliminary risk assessment

Feasibility studies

The feasibility study is a useful mechanism for setting forth a description of the project, the goals of the project sponsor, sensitivities of the project to various construction, start-up and operating risks, an analysis of financing alternatives and credit enhancement. It will include estimated capital needs, debt service capabilities, revenue projections from output sales, operating costs and market projections. Typically, variables such as fuel cost fluctuation, interest rates, currency exchange rates and others are examined in alternative scenarios.

The study enables the sponsors and lenders to analyze the potential of the project before any party unnecessarily commits resources when the project is not economically feasible. The study must, of course, conclude that the project will have sufficient viability to pay debt service, operations and maintenance costs provide a return on equity, and, if necessary, provide for contingencies. The feasibility study is useful in that it can be analyzed by various legal, financial and technical experts to establish whether the project if viable or not.

Due diligence

Due diligence in project financing is an important process for risk identification. It encompasses legal, technical, environmental and financial matters, and is designed to detect events that might result in total or partial project failure. Participants involved in this process, besides the project sponsors, are lawyers, construction companies, fuel consultants, market consultants, insurance consultants, financial advisers and environmental consultants. The level of due diligence undertaken involves considerations of time available, cost and the type of project.

Risk periods

There are three main risk periods in a project financing:

Engineering and construction phase risks

This first stage is when the risk is highest – funds begin to flow from the financiers to the project entity. No cash flow is being generated from the project, however, no interest can be paid and in many financings the borrower is allowed to ‘roll up’ interest or draw down further funds to make interest payments. The length of this phase can vary from several months to several years. The lenders become more exposed as funds are drawn down but cash flows have yet to be generated.

Risks associated with the project during the construction phase include :

Start-up risks

During the start-up phase the banks need to be satisfied that the project will operate at the costs and according to the specifications agreed at the outset. The phase is especially significant if the loan becomes ‘non-recourse’ once the project has been completed.

The basis on which conversion takes place will require much thought and negotiation prior to the loan being signed. At this point, however, it is important to understand that the start-up phase may last for a period of many months. The technical assessment of a project therefore includes an evaluation of the facility’s acceptance testing and start-up procedures, since they are an integral part of construction completion.

A potential conflict of interest and therefore risk arises from the need to start commercial operations versus the need to get the project to pass its long-term reliability test. Financial pressures, which often occur near the end of the construction phase, to ‘get the job done’ may prompt the sponsor to accept a compromised performance test in an effort to generate cash flow as soon as possible.

Operational risks

Once the project is complete the lenders in many project financings become dependent on stable cash flows to service the project loans. The lending risk is similar to the risks encountered in commercial loans in similar businesses. The future cash flows of the project company are subject to the usual operating costs, raw material costs, regulatory risks and markets for the products.

Risks associated with the project during the operational phase include :

Financial risks

The project is now operating as a regular operating company and cash flow are being generated. As long as the project is performing according to plan, the risks to the lenders will reduce from their peak in the start-up phase. The borrower should not only be able to make interest payments but also repay the principal. As long as correct financial planning has been carried out, the company should be in a position to service debt. In a typical project finance transaction the banks will ensure that they have security over the sales proceeds.

Once the project is on stream, the project financial advisers should identify and mitigate for any risks that may occur outside of the project and scope of the project sponsor’s control. Some of these risks are :

Country/political risks

One can find that country risk can arise through different paths :

Therefore, when we speak about country risk, we mean the exposure to a loss in cross-border lending (of different types) due to events more or less under the control of the government.

Typical examples of political risk are :

Legal risks

By legal risk is meant that the application of laws in the host country may not necessarily be consistent with that of the lender’s home countries, and that judgments may yield results substantially different than those expected. It is therefore essential that project lenders review the legal risks at an early stage. Some banks may require the host country to pass specific legislation favorable to a project, which lends a new meaning to ‘interference in domestic affairs’! Getting such legislation implemented no doubt requires numerous cash commissions to key government officials to accelerate lengthy procedures. A breakdown of legal risks includes :

Environmental, regulatory and approval risks

Obtaining all the requisite approvals for a project is indispensable to its success. Indeed, all permissions should be obtained prior to setting in place the facility and forwarding funds. It is essential that these be included as conditions precedent in the facility documentation. Likewise for environmental and regulatory issues: these should be spelled out clearly in the loan agreement since there is a risk that other regulatory and environmental risks, may live to haunt the lenders if the project should fail and decontamination costs have to be borne by the lender who takes possession of the security in order to satisfy the outstanding loan.

Force majeure

Force majeure means that entities are not responsible for performance shortfalls caused by unanticipated events outside their control. Project finance transactions are particularly vulnerable to force majeure risks due to the complexity of the transactions, the numerous participants in the project, the physical nature of construction activity, associated technical and performance risks, and impact of geographic distance and transport of raw materials.

Sponsors typically will not want to assume those risks and the financing parties should not accept these risks. It is therefore important to segregate risks which are those under the borrower’s remit (technical, construction) against natural risks (floods and earthquakes, civil disturbances, strikes, or changes of law). While companies may be exempt from force majeure risks, it should be noted that they may still lead to a default depending on its severity.

The unpredictability of force majeure events makes effective mitigation difficult. Projects that show linearity in design or operations, such as toll roads, pipelines, or assembly line production, tend to be less at risk of operational force majeure accidents than operations which are complex (e.g. chemical plants, LNG facilities, refineries, and nuclear power plants).

Feasibility studies

The feasibility study is a useful mechanism for setting forth a description of the project, the goals of the project sponsor, sensitivities of the project to various construction, start-up and operating risks, an analysis of financing alternatives and credit enhancement. It will include estimated capital needs, debt service capabilities, revenue projections from output sales, operating costs and market projections. Typically, variables such as fuel cost fluctuation, interest rates, currency exchange rates and others are examined in alternative scenarios.

The study enables the sponsors and lenders to analyze the potential of the project before any party unnecessarily commits resources when the project is not economically feasible. The study must, of course, conclude that the project will have sufficient viability to pay debt service, operations and maintenance costs provide a return on equity, and, if necessary, provide for contingencies. The feasibility study is useful in that it can be analyzed by various legal, financial and technical experts to establish whether the project if viable or not.

Due diligence

Due diligence in project financing is an important process for risk identification. It encompasses legal, technical, environmental and financial matters, and is designed to detect events that might result in total or partial project failure. Participants involved in this process, besides the project sponsors, are lawyers, construction companies, fuel consultants, market consultants, insurance consultants, financial advisers and environmental consultants. The level of due diligence undertaken involves considerations of time available, cost and the type of project.

Risk periods

There are three main risk periods in a project financing:

- engineering and construction;

- start-up;

- operational.

Engineering and construction phase risks

This first stage is when the risk is highest – funds begin to flow from the financiers to the project entity. No cash flow is being generated from the project, however, no interest can be paid and in many financings the borrower is allowed to ‘roll up’ interest or draw down further funds to make interest payments. The length of this phase can vary from several months to several years. The lenders become more exposed as funds are drawn down but cash flows have yet to be generated.

Risks associated with the project during the construction phase include :

- Sponsor risk. Sponsor risk is closely associated with completion risk. Regarding equity commitment, lenders will normally require a contribution of anything from 15% to 50% of the project cost to ensure the sponsor’s continued commitment. In addition, lenders prefer to work with corporate sponsors that have substantial technical expertise and financial depth.

- Pre-completion risk. The engineering and design review focuses on the suitability of the technology and design chosen for the project. These objectives recognize that construction risk levels vary among different technologies and the size of certain projects. Banks may well hesitate to finance projects using unproven technology.

- Siting and permitting. Site and permitting risks are often linked to political risk, and can present a more difficult area of analysis. Regulations and legislation in some jurisdictions can leave continuous openings for project opponents to stop projects for reasons related, or unrelated, to siting concerns.

- Completion risks. In essence, the risk is whether or not the project can be built on time, on budget and in accordance with the applicable specifications and design criteria.

- Experience and resources of D&B contractor. The contractor’s experience, reputation and reliability should provide an indicator of the possibility of achieving timely completion of the project at the stated price.

- Building materials. A project finance risk often overlooked. Of particular concern is the impact of import and export laws when the project is either located abroad or where imported materials are contemplated for construction.

- Facility site. Pre-existing conditions on the project site can affect both construction and long-term operations, especially if the site has hazardous waste problems.

- Construction of related facilities. International projects, particularly in developing countries, often require simultaneous construction of facilities related to the project. These various facilities will all be interrelated and may need simultaneous construction to ensure project success.

- Cost overruns. The risk that construction costs start to increase uncontrollably is perhaps the most important risk for the participants in a project financing. This may result in liquidity crises, as well as impact on long term cash flows.

- Completion delays. Construction delays can have a similar impact to cost overruns, as it may affect the scheduled flow of project revenues and result in higher than expected financing costs.

Start-up risks

During the start-up phase the banks need to be satisfied that the project will operate at the costs and according to the specifications agreed at the outset. The phase is especially significant if the loan becomes ‘non-recourse’ once the project has been completed.

The basis on which conversion takes place will require much thought and negotiation prior to the loan being signed. At this point, however, it is important to understand that the start-up phase may last for a period of many months. The technical assessment of a project therefore includes an evaluation of the facility’s acceptance testing and start-up procedures, since they are an integral part of construction completion.

A potential conflict of interest and therefore risk arises from the need to start commercial operations versus the need to get the project to pass its long-term reliability test. Financial pressures, which often occur near the end of the construction phase, to ‘get the job done’ may prompt the sponsor to accept a compromised performance test in an effort to generate cash flow as soon as possible.

Operational risks

Once the project is complete the lenders in many project financings become dependent on stable cash flows to service the project loans. The lending risk is similar to the risks encountered in commercial loans in similar businesses. The future cash flows of the project company are subject to the usual operating costs, raw material costs, regulatory risks and markets for the products.

Risks associated with the project during the operational phase include :

- Operating/performance risk. Operational risk is the risk that normal ongoing operations will fail to generate the cash flow required to run the project and service debt. This is why banks tend to be reassured if the project operations will be taken on by experienced third party operations and maintenance contractors, on a fixed cost basis.

- Raw material/supply risk. This is another key risk category: input and supply risk relates to obtaining the requisite energy and raw materials for the project. The flow of these inputs must be assured, and within the parameters set by the project financial projections. This is why it is important to identify alternate sources should they be needed.

- Offtake and sales risk. The offtake and sales risk is the risk that the project will fail to generate sufficient cash flow. This is why the off-take risk, or the sales, is the key risk that banks will look at. Offtake agreements such as long term contracts to purchase electricity at fixed prices will substantially eliminate any sales volatility or instability, and will be considered as a positive element by the banks.

- Counter-party risk. Counter-parties include parties such as the contractor, bank providing bonds, purchasers or off-takers, insurance companies, etc. If any of these parties defaults in the performance of their respective obligations, then the project may run into difficulties.

- Technology/obsolescence risk. Banks tend to want to avoid new technology risk until it becomes proven technology. However, project sponsors cannot ignore new technology since often the success of such projects resides in cost efficiencies arising from new technology. Therefore, as a minimum, the contractor must have experience with the technology and provide adequate guarantees to support the underlying debt.

Financial risks

The project is now operating as a regular operating company and cash flow are being generated. As long as the project is performing according to plan, the risks to the lenders will reduce from their peak in the start-up phase. The borrower should not only be able to make interest payments but also repay the principal. As long as correct financial planning has been carried out, the company should be in a position to service debt. In a typical project finance transaction the banks will ensure that they have security over the sales proceeds.

Once the project is on stream, the project financial advisers should identify and mitigate for any risks that may occur outside of the project and scope of the project sponsor’s control. Some of these risks are :

- Foreign exchange (FX) risk. If all project inputs are denominated on one currency, there will be no FX risk. If this is not the case, the lender may need to assume some of the risk via multi-currency loans, which give the borrower an option, based on a fixed FX rate, of repaying in different currencies. Lenders can sometimes hedge these risks using appropriate hedging instruments.

- Interest rate risk. Project financings may rely on floating interest rate loans. Most project financings remove interest rate risk by financing with fixed interest rate debt. Some projects however have incorporated debt with interest rates tied to a floating reference rate. Where projects chose to use floating rate debt, the financial projections should demonstrate that in a high interest rate scenario the project will still have enough available cash flow to service financing commitments.

- Inflation risk. This risk exists when certain of the inputs can be subjected to price inflation (e.g. rising fuel costs). In such cases, the project sponsor must be able to pass on these price increases to customers. If the project output is a product whose price levels are fixed by the government (e.g. electricity cost), the ability to pass on the cost increase will be limited. Similar risks exist when the inputs are denominated in one currency and the project outputs in another. Thus it is important to identify any such risks and the ability to pass them on to the customers.

- Liquidity risk. Projects should be able to demonstrate the ability to generate sufficient cash to fund major maintenance reserve funds. If not, a potential liquidity risk exists. Financial projections should therefore demonstrate that an adequate cash flow, enabling the company to generate enough cash to fund ongoing operations and fund reserves, exists.

Country/political risks

One can find that country risk can arise through different paths :

- Political events such as war, ideology, neighboring countries, political unrest, revolution, etc. comprise political risk. Political risk is the risk that a country is not willing or able, due to political reasons, to service/repay its foreign debt/obligations.

- Economic factors such as internal and external debt levels, GDP growth, inflation, import dependency etc. comprise economic risk. Economic risk is the risk that a country is not willing or able, due to economic reasons, to service/repay its foreign debt/obligations.

- Social factors such as religious, ethnic, or class conflict, trade unions, inequitable income distribution etc. comprise social risk. Social risk is the risk that a country is not able, or is unwilling, to repay its foreign debt/obligations due to social reasons.

Therefore, when we speak about country risk, we mean the exposure to a loss in cross-border lending (of different types) due to events more or less under the control of the government.

Typical examples of political risk are :

- expropriation or nationalization of project assets;

- failure of a government department to grant a necessary consent or permit;

- imposition of increased taxes and tariffs;

- withdrawal of valuable tax holidays and/or concessions;

- imposition of exchange controls, restricting the transfer of funds to outside the host country;

- changes in law adversely impacting project parties’ obligations with respect to the project.

Legal risks

By legal risk is meant that the application of laws in the host country may not necessarily be consistent with that of the lender’s home countries, and that judgments may yield results substantially different than those expected. It is therefore essential that project lenders review the legal risks at an early stage. Some banks may require the host country to pass specific legislation favorable to a project, which lends a new meaning to ‘interference in domestic affairs’! Getting such legislation implemented no doubt requires numerous cash commissions to key government officials to accelerate lengthy procedures. A breakdown of legal risks includes :

- Identifying and establishing applicable laws and jurisdiction. Project finance requires the establishment of a stable legal framework required for ongoing business operation. It is therefore important to identify the strengths and weaknesses of a given legal system and plan for the shortcomings appropriately.

- Security. In project finance – particularly where recourse is limited – the ability to take effective security can assume crucial importance. Laws on the taking and enforcement of security, particularly in the case of moveable assets, cash flows and contractual rights (such as receivables) might be less than satisfactory, and should be evaluated.

- Permits and licensing. There is a risk when permits and licenses must be obtained and renewed before the plant will operate. Effectively, this means that the lenders are assuming the risk that the requisite permits and licenses will be obtained in a reasonable time should the sponsors not provide any commitment to assume the costs arising from such delays.

- Limited rights to appeal. The local lawyers and the judiciary might lack the requisite experience to judge project related disputes; resulting judgments may therefore be slower than expected and, yield unpredictable results.

- Enforceability of contracts. Even if a project is supported by take-or-pay contracts with adequate escalation clauses, enforceability may very well be an open question, as well as the ability or motivation of the contracting party to honor its contractual commitments.

- Structural risk. This is the risk that the interrelations of project elements may not function as initially envisaged. Complex projects can involve complex and interlocking documents, which may be flawed. Allegiances moreover can shift during the life of a contract.

Environmental, regulatory and approval risks

Obtaining all the requisite approvals for a project is indispensable to its success. Indeed, all permissions should be obtained prior to setting in place the facility and forwarding funds. It is essential that these be included as conditions precedent in the facility documentation. Likewise for environmental and regulatory issues: these should be spelled out clearly in the loan agreement since there is a risk that other regulatory and environmental risks, may live to haunt the lenders if the project should fail and decontamination costs have to be borne by the lender who takes possession of the security in order to satisfy the outstanding loan.

- Environmental risk. Environmental risk is increasingly becoming an issue of public concern, and is increasingly being subject to legislation controlling the adverse impact projects and the emissions, waste, hazardous substances and inefficient use of energy they may generate. Lenders need to insulate themselves from these risks.

- Regulatory, licensing and permit risks. It is essential that all regulatory, licensing and permits issues are met at the outset of the project since if there are any difficulties and the lenders take possession of the security when a project fails to perform, this may cause difficulties. In the absence of appropriate governmental permits, this may result in fines. In the case of regulatory and licensing issues, the lenders may find themselves liable for the legal consequences of pollution caused by that project.

- Public opposition. Public opposition to a project can become an unwelcome nuisance to bankers. Public opposition (via procedural challenges of permits and approvals) can result in costly delays to the project. The feasibility study should therefore consider public opposition as one factor in the chance for project success.

Force majeure

Force majeure means that entities are not responsible for performance shortfalls caused by unanticipated events outside their control. Project finance transactions are particularly vulnerable to force majeure risks due to the complexity of the transactions, the numerous participants in the project, the physical nature of construction activity, associated technical and performance risks, and impact of geographic distance and transport of raw materials.

Sponsors typically will not want to assume those risks and the financing parties should not accept these risks. It is therefore important to segregate risks which are those under the borrower’s remit (technical, construction) against natural risks (floods and earthquakes, civil disturbances, strikes, or changes of law). While companies may be exempt from force majeure risks, it should be noted that they may still lead to a default depending on its severity.

The unpredictability of force majeure events makes effective mitigation difficult. Projects that show linearity in design or operations, such as toll roads, pipelines, or assembly line production, tend to be less at risk of operational force majeure accidents than operations which are complex (e.g. chemical plants, LNG facilities, refineries, and nuclear power plants).

Let's take a closer look now at the possible mitigation options in PPPs.

Follow this link : Mitigation and risk allocation.

Follow this link to Summary.

Follow this link : Mitigation and risk allocation.

Follow this link to Summary.

In case you need more information, or are eager to get into the details of Project Finance, I recommend the following reads , that I personally bought as to create the summarized information of this Project Finance website (Amazon links) :

|

|