25. Understanding Income Statements

A. Components of the income statement and alternative presentation formats :

The income statement shows an entity’s revenues, expenses, gains and losses during the reporting period.

A multi-step income statement provides a subtotal for gross profit and a single-step income statement does not.

Multi-step income statement :

Revenue

- Cost of goods sold

= Gross profit

- Selling, general, and administrative expense

- Depreciation expense

= Operating profit (EBIT)

- Interest expense

= Income before tax (EBT)

- Provision for income taxes

= Income from continuing operations

- Earnings (losses) from discontinued operations, net of tax

= Net income

Gross profit is equal to sales minus cost of goods sold. Cost of goods sold includes the direct costs of producing a product or service such as raw materials, direct labor and overhead.

B. General principles of revenue recognition and accrual accounting, specific revenue recognition applications :

According to the FASB, revenue is recognized when in the income statement when realized or realizable and earned. The SEC provides additional guidance by listing four criteria to determine whether revenue should be recognized :

- There is evidence of an arrangement between the buyer and seller.

- The product has been delivered or the service has been rendered.

- The price is determined or determinable.

- The seller is reasonably sure of collecting money.

In some cases, revenue may be recognized before delivery occurs or even after delivery takes place:

Long-term contracts :

When the outcome of a long-term contract can be reliably estimated, the percentage-of-completion method is used under both IFRS and U.S. GAAP. The percentage-of-completion is measured by the total cost incurred to date divided by the total expected cost of the project.

When the outcome cannot be reliably estimated :

- Under U.S. GAAP, the completed-contract method is used. Revenue, expense and profit are recognized only when the contract is complete.

- Under IFRS, the revenue is recognized to the extent of contract costs, costs are expensed when incurred, and profit is recognized only at completion.

The percentage-of-completion method is more aggressive than the completed-contract method (more conservative).

Installment sales :

An installment sale occurs when a firm finances a sale and payments are expected to be received over an extended period:

- If collectability is certain, revenue is recognized at the time of the sale using the normal recognition criteria.

- If collectability cannot be reasonably estimated, the installment method is used. Profit is recognized as cash is collected. Profit is equal to the cash collected during the period multiplied by the total expected profit as a percentage of sales.

- If collectability is highly uncertain, the cost recovery method is used. Profit is recognized only when cash collected exceeds costs incurred.

Barter transactions :

In a barter transaction, two parties exchange goods or services without cash payment. Revenue from barter transactions can only be recognized if its fair value can be estimated from historical data on similar non-barter transactions.

C. Implications of revenue recognition principles for financial analysis:

Firms must disclose their revenue recognition policies in the financial footnotes.

Analysts must consider two points when analyzing a firm’s revenue :

- How conservative are the firm’s recognition policies.

- The extent to which the firm’s policies rely on judgment and estimates.

D. General principles of expense recognition, specific applications and implications for financial analysis :

Accrual accounting is based on the matching principle, under which revenues are recognized in the same period that the expenses are incurred to generate those revenues.

Not all expenses can be directly tried to revenue generation. These costs are known as period costs. Example: administration costs are expensed in the period incurred.

Inventory expense recognition :

- If a firm can identify which items were sold and which items remain in inventory, it can use the specific identification method. Example: auto dealer.

- Under the First-In, First-Out (FIFO), the first item purchased is assumed to be the first item sold. The cost of the most recent purchases is used to calculate ending inventory.

- Under the Last-In, First-Out (LIFO), the last item purchased is assumed to be the first item sold. The costs of beginning inventory and earlier purchases are assigned to ending inventory.

- The weighted average cost method makes no assumption about the physical flow of the inventory. The cost per unit is calculated by dividing cost of available goods by total units available, and this average cost is used to determine both cost of goods sold and ending inventory.

The FIFO cost method best approximates the physical flow of goods if customers typically purchase units in the order they are produced, such as goods with limited shelf life (food products, movies...).

LIFO best approximates the flow of goods if customers purchase units from the top of the stack. LIFO is appropriate for inventory that does not deteriorate with age. In the U.S., LIFO is popular because of its income tax benefits. In an inflationary environment, LIFO results in higher cost of goods sold. Higher cost of goods sold results in lower taxable income and, therefore, lower income taxes.

FIFO and weighted average cost are permitted under both U.S. GAAP and IFRS. LIFO is allowed under U.S. GAAP but prohibited under IFRS.

Depreciation expense recognition :

The allocation of cost over an asset’s life is known as depreciation (tangible assets), depletion (natural resources), or amortization (intangible assets). Three methods are usually used for determining depreciation :

- Straight-line (SL) depreciation: Allocates an equal amount of depreciation each year over the asset’s useful life.

- Accelerated depreciation: Speeds up the recognition of depreciation expense in a systematic way to recognize more depreciation expense in the early years of the asset’s life and less depreciation expense in the later years of its life.

- The declining balance (diminishing balance) method: Applies a constant rate of depreciation to an asset’s book value each year. The most common method is the double-declining balance (DDB) :

Amortization expense recognition :

Most firms use the straight-line method to calculate annual amortization expense for financial reporting.

Under IFRS and U.S. GAAP, intangible assets with indefinite lives (goodwill) are not amortized but are tested for impairment at least annually.

E. Financial reporting treatment and analysis of non-recurring items and changes in accounting standards :

Non-recurring items :

A discontinued operation is one that management has decided to dispose of, but either has not yet done so, or has disposed of in the current year after the operation has generated income or losses. Results of discontinued operations are reported below income from continuing operations, net of tax, from the date the decision of the operations is made. These results are segregated because they likely are non-recurring and do not affect future net income.

Unusual or infrequent items. Either unusual in nature or infrequent in occurrence, not both. They are reported as a component of net income from continuous operations. Examples include :

Extraordinary items. Under U.S. GAAP, an extraordinary item is a material transaction or event that is both unusual and infrequent. Examples include :

IFRS does not allow extraordinary items to be separated from operating results in the income statement.

Change in accounting standards:

A change in accounting principle refers to a change from one GAAP or IFRS method to another. This requires retrospective application: all of the prior-period financial statements are restated to reflect the change.

A change in accounting estimate (useful life) is the result of a change in management’s judgment, usually due to new information. This change is applied prospectively and does not require restatement.

A change from an incorrect accounting method to one that is acceptable under GAAP or IFRS or the correction of an accounting error is reported as a prior-period adjustment (PPA).

F. Difference between operating and non-operating components of IS :

Operating income is generated from the firm’s normal business operations. For a non-financial firm, income that results from investing or financing transactions is classified as non-operating income, while it is operating income for a financial firm since its business operations include investing in and financing securities.

Under U.S. GAAP, restructuring costs are operating items.

G. Calculation of EPS (basic and dilutive) and its interpretation for simple and complex capital structures :

Earnings per share (EPS) is one of the most used corporate profitability performance measures for publicly-traded firms (nonpublic companies are not required to report EPS data). EPS is reported only for shares of common stock.

A simple capital structure is one that contains no potentially dilutive securities. It contains only common stock, nonconvertible debt, and nonconvertible preferred stock. These firms only report basic EPS.

A complex capital structure contains potentially dilutive securities such as options, warrants, or convertible securities. These firms must report both basic and diluted EPS.

Basic EPS :

Most firms use the straight-line method to calculate annual amortization expense for financial reporting.

Under IFRS and U.S. GAAP, intangible assets with indefinite lives (goodwill) are not amortized but are tested for impairment at least annually.

E. Financial reporting treatment and analysis of non-recurring items and changes in accounting standards :

Non-recurring items :

A discontinued operation is one that management has decided to dispose of, but either has not yet done so, or has disposed of in the current year after the operation has generated income or losses. Results of discontinued operations are reported below income from continuing operations, net of tax, from the date the decision of the operations is made. These results are segregated because they likely are non-recurring and do not affect future net income.

Unusual or infrequent items. Either unusual in nature or infrequent in occurrence, not both. They are reported as a component of net income from continuous operations. Examples include :

- Gain or losses from the sale of assets or part of a business.

- Impairments, write-offs, write-downs, restructuring costs.

- Integration expenses.

Extraordinary items. Under U.S. GAAP, an extraordinary item is a material transaction or event that is both unusual and infrequent. Examples include :

- Losses from the expropriation of assets.

- Gains or losses from early retirement of debt.

- Uninsured losses from natural disasters (Earthquakes, eruptions...)

IFRS does not allow extraordinary items to be separated from operating results in the income statement.

Change in accounting standards:

A change in accounting principle refers to a change from one GAAP or IFRS method to another. This requires retrospective application: all of the prior-period financial statements are restated to reflect the change.

A change in accounting estimate (useful life) is the result of a change in management’s judgment, usually due to new information. This change is applied prospectively and does not require restatement.

A change from an incorrect accounting method to one that is acceptable under GAAP or IFRS or the correction of an accounting error is reported as a prior-period adjustment (PPA).

F. Difference between operating and non-operating components of IS :

Operating income is generated from the firm’s normal business operations. For a non-financial firm, income that results from investing or financing transactions is classified as non-operating income, while it is operating income for a financial firm since its business operations include investing in and financing securities.

Under U.S. GAAP, restructuring costs are operating items.

G. Calculation of EPS (basic and dilutive) and its interpretation for simple and complex capital structures :

Earnings per share (EPS) is one of the most used corporate profitability performance measures for publicly-traded firms (nonpublic companies are not required to report EPS data). EPS is reported only for shares of common stock.

A simple capital structure is one that contains no potentially dilutive securities. It contains only common stock, nonconvertible debt, and nonconvertible preferred stock. These firms only report basic EPS.

A complex capital structure contains potentially dilutive securities such as options, warrants, or convertible securities. These firms must report both basic and diluted EPS.

Basic EPS :

The current year’s preferred dividends are subtracted from net income because EPS refers to the per-share earnings available to common shareholders.

The weighted average number of common shares outstanding is the number of shares outstanding during the year, weighted by the portion of the year they were outstanding.

A stock dividend is the distribution of additional shares to each shareholder in an amount proportional to their current number of shares. If a 10% stock dividend is paid, the holder of 100 shares would receive 10 additional shares.

A stock split refers to the division of each ‘old’ share into a specific number of ‘new’ shares. The holder of 100 shares will have 200 shares after a 2-for-1 split or 150 shares after a 3-for-2 split.

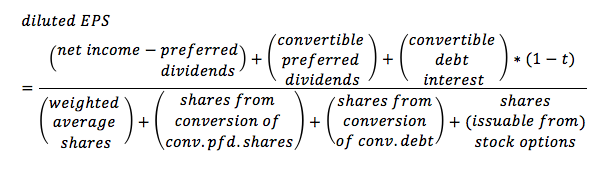

Diluted EPS :

The diluted EPS equation is :

The weighted average number of common shares outstanding is the number of shares outstanding during the year, weighted by the portion of the year they were outstanding.

A stock dividend is the distribution of additional shares to each shareholder in an amount proportional to their current number of shares. If a 10% stock dividend is paid, the holder of 100 shares would receive 10 additional shares.

A stock split refers to the division of each ‘old’ share into a specific number of ‘new’ shares. The holder of 100 shares will have 200 shares after a 2-for-1 split or 150 shares after a 3-for-2 split.

Diluted EPS :

The diluted EPS equation is :

In there are dilutive securities, then the numerator must be adjusted as follows :

When the firm has dilutive securities outstanding, the denominator is the basic EPS denominator adjusted for the equivalent number of common shares that would be created by the conversion of all dilutive securities outstanding, with each one considered separately to determine if it’s dilutive.

Stock options and warrants are dilutive only when their exercise prices are less than the average market price of the stock over the year.

The treasury stock method assumes any funds received by the company from the exercise of the options are used to purchase share (not sell shares) of the company’s common stock in the market at the average market price.

H. Difference between dilutive and anti dilutive securities :

Dilutive securities are stock options, warrants, convertible debt, or convertible preferred stock that would decrease EPS if exercised or converted to common stock.

Antidilutive securities are stock options, warrants, convertible debt, or convertible preferred stock that would increase EPS if exercised or converted to common stock.

I. Converting income statements to common-size income statements :

A vertical common-size income statement expresses each category of the income statement as percentage of revenue. This allows for comparison of income statement items over time and across firms.

In most cases, expressing expenses as a percentage of revenue is appropriate. One exception is income tax expense. Tax expense is more meaningful when expressed as a percentage of pretax income. The result is known as the effective tax rate.

J. Financial ratios based on income statement :

Gross profit margin is the ratio of gross profit (revenue minus COGS) to revenue. It can be increased by raising prices or reducing production costs.

Another popular margin ratio is net profit margin. Net profit margin is the ratio of net income to revenue. It measures the profit generated after considering all expenses. Like gross profit margin, it should be compared over time and with industry peers.

Operating profit margin = Operating profit / Revenue

Pretax margin = Pretax profit / Revenue

K. Describe comprehensive income :

Comprehensive income is the sum of net income and other comprehensive income. It measures all changes in equity other than those from transactions with shareholders.

Comprehensive income is a more inclusive measure that includes all changes in equity except for owner contributions and distributions.

L. Describe other comprehensive income :

Other comprehensive income includes transactions that are not included in net income, such as:

Available-for-sale securities are investments securities that are not expected to be held to maturity or sold in the near term. They are reported on the balance sheet at fair value. The unrealized gains and losses (changes in fair value before the securities are sold) are reported as other comprehensive income.

Under IFRS, firms can choose to report certain long-lived assets at fair value rather than historical cost. In this case, the changes in fair value are also included in other comprehensive income.

- If convertible preferred stock is dilutive, the convertible preferred dividends must be added to earnings available to common shareholders.

- If convertible debt are dilutive, then the bonds’ after-tax interest expense is not considered an interest expense for diluted EPS. Hence, interest expense multiplied by (1-tax rate) must be added back to the numerator.

When the firm has dilutive securities outstanding, the denominator is the basic EPS denominator adjusted for the equivalent number of common shares that would be created by the conversion of all dilutive securities outstanding, with each one considered separately to determine if it’s dilutive.

Stock options and warrants are dilutive only when their exercise prices are less than the average market price of the stock over the year.

The treasury stock method assumes any funds received by the company from the exercise of the options are used to purchase share (not sell shares) of the company’s common stock in the market at the average market price.

H. Difference between dilutive and anti dilutive securities :

Dilutive securities are stock options, warrants, convertible debt, or convertible preferred stock that would decrease EPS if exercised or converted to common stock.

Antidilutive securities are stock options, warrants, convertible debt, or convertible preferred stock that would increase EPS if exercised or converted to common stock.

I. Converting income statements to common-size income statements :

A vertical common-size income statement expresses each category of the income statement as percentage of revenue. This allows for comparison of income statement items over time and across firms.

In most cases, expressing expenses as a percentage of revenue is appropriate. One exception is income tax expense. Tax expense is more meaningful when expressed as a percentage of pretax income. The result is known as the effective tax rate.

J. Financial ratios based on income statement :

Gross profit margin is the ratio of gross profit (revenue minus COGS) to revenue. It can be increased by raising prices or reducing production costs.

Another popular margin ratio is net profit margin. Net profit margin is the ratio of net income to revenue. It measures the profit generated after considering all expenses. Like gross profit margin, it should be compared over time and with industry peers.

Operating profit margin = Operating profit / Revenue

Pretax margin = Pretax profit / Revenue

K. Describe comprehensive income :

Comprehensive income is the sum of net income and other comprehensive income. It measures all changes in equity other than those from transactions with shareholders.

Comprehensive income is a more inclusive measure that includes all changes in equity except for owner contributions and distributions.

L. Describe other comprehensive income :

Other comprehensive income includes transactions that are not included in net income, such as:

- Foreign currency translation gains and losses.

- Adjustments for minimum pension liability.

- Unrealized gains and losses from cash flow hedging derivatives.

- Unrealized gains and losses from available-for-sale securities.

Available-for-sale securities are investments securities that are not expected to be held to maturity or sold in the near term. They are reported on the balance sheet at fair value. The unrealized gains and losses (changes in fair value before the securities are sold) are reported as other comprehensive income.

Under IFRS, firms can choose to report certain long-lived assets at fair value rather than historical cost. In this case, the changes in fair value are also included in other comprehensive income.

|

|