32. Non-current (long-term) liabilities

Bond terminology :

A bond is a contractual promise between a borrower (the bond issuer) and a lender (the bondholder) that obligates the bond issuer to make payments to the bondholder over the term of the bond. Typically, two types of payments are involved : (1) periodic interest payments, and (2) repayment of principal at maturity.

The face value, also known as the maturity value or par value, is the amount of principal that will be paid to the bondholder at maturity. The face value is used to calculate the coupon payments.

The coupon rate is the interest rate stated in the bond that is used to calculate the coupon payments. The coupon rate is typically fixed for the term of the bond.

The coupon payments are the periodic interest payments to the bondholders and are calculated by multiplying the face value by the coupon rate.

The effective rate of interest is the interest rate that equates the present value of the future cash flows of the bond and the issue price. The effective rate is the market rate of interest required by bondholders and depends on the bond’s risks, as well as the overall structure of interest rates and the timing of the bond’s cash flows. The market rate of interest on a firm’s bonds will likely change over the bond’s life, which changes the bond’s market value as well.

The balance sheet liability of a bond is equal to the present value of its remaining cash flows (coupon payments and face value), discounted at the market rate of interest at issuance. At maturity, the liability will equal the face value of the bond. The balance sheet liability is also know as the book value or carrying value of the bond.

The interest expense reported in the income statement is calculated by multiplying the book value of the bond liability at the beginning of the period by the market rate of interest of the bond when it was issued.

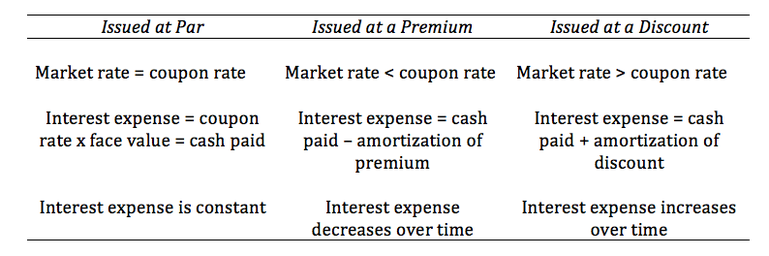

At the date of issuance, the market rate of interest may be equal to, less than, or greater than the coupon rate :

- When the market rate is equal to the coupon rate, the bond is a par bond (priced at par value).

- When the market rate is greater than the coupon rate, the bond is a discount bond (priced below par).

- When the market rate is less than the coupon rate, the bond is a premium bond (priced above par).

A. Determine the initial recognition, initial measurement, and subsequent measurement of bonds :

Bonds issued at par :

When a bond is issued at par, the bond’s yield at issuance is equal to the coupon rate. In this case, the present value of the coupon payments plus the present value of the face amount is equal to the par value. The effects on the financial statements are straightforward :

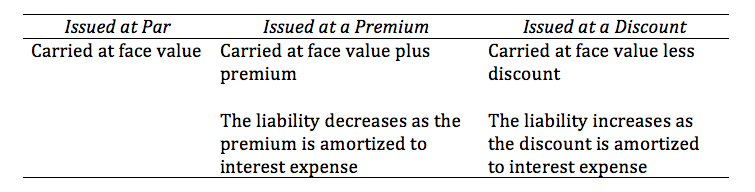

- On the balance sheet, assets and liabilities increase by the bond proceeds (face value). The book value of the bond liability will not change over the term of the bond.

- On the income statement, interest expense for the period is equal to the coupon payment because the yield at issuance and the coupon rate are the same.

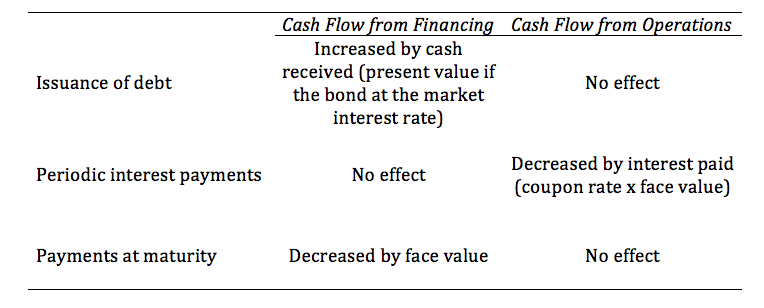

- On the cash flow statement, the issue proceeds are reported as a cash inflow from financing activities and the coupon payments are reported as cash outflows from operating activities (under U.S. GAAP; they may be reported as CFO or CFF outflows under IFRS). At maturity, repayment of the face value is reported as cash outflow from financing activities.

Bond issued at a discount or premium :

When the bond’s yield at issuance is not equal to the coupon rate, the proceeds received (the present value of the coupon payments plus the present value of the face value) are not equal to par value. In this case, the bond is issued at a premium or a discount. The premium or discount at the issue fate is usually relatively small for coupon bonds.

If the coupon rate is less than the bond’s yield, the proceeds received will be less than the face value. The difference is known as a discount.

If the coupon rate is greater than the bond’s yield, the bond price and the proceeds received will be greater than face value. We refer to such bonds as premium bonds.

Balance sheet measurement :

When a company issues a bond, assets and liabilities both initially increase by the bond proceeds. At any point in time, the book value of the bond will equal the present value of the remaining future cash flows (coupon payments and face value) discounted at the bond’s yield at issuance.

Interest expense and the book value of a bond liability are calculated using the bond’s yield at the time it was issued, not its yield today.

A premium bond is reported on the balance sheet at more than its face value. As the premium is amortized (reduced), the book value of the bond liability will decrease until it reaches the face value of the bond at maturity.

A discount bond is reported on the balance sheet at less than its face value. As the discount is amortized, the book value of the bond liability will increase until it reaches face value at maturity.

B. Effective interest method, interest expense, amortization of bond discounts/premiums, and interest payments :

For a bond issued at a premium or discount, interest expense and coupon payments are not equal. Interest expense includes amortization of any discount or premium. Using the effective interest rate method, interest expense is equal to the book value of the bond liability at the beginning of the period, multiplied by the bond’s yield at issuance.

- For a premium bond, interest expense is less than the coupon payment (yield < coupon rate). The difference between interest expense and the coupon payment is the amortization of the premium. The premium amortization is subtracted each period from the bond liability on the balance sheet. Thus, interest expense will decrease over time as the bond liability decreases.

- For a discount bod, interest expense is greater than the coupon payment (yield > coupon rate). The difference between interest expense and the coupon rate is the amortization of the discount. The amortization of the discount each period is added to the bond liability on the balance sheet. Therefore, interest expense will increase over time as the bond liability increases.

The effective interest rate method of amortizing a discount or premium is required under IFRS. Under U.S. GAAP, the effective interest rate method is preferred, but the straight-line method is allowed if the results are not materially different. The straight-line method is similar to straight-line depreciation in that the total discount or premium at issuance is amortized by equal amounts each period over the life of the bond.

While coupon interest is paid in cash, amortization is a noncash item. When presenting the cash flow statement using the indirect method, net income must be adjusted to remove the effects of any amortization of a discount or premium in order to calculate cash flow from operations.

Zero-coupon bonds make no periodic interest payments. A zero-coupon bond, also known as a pure-discount bond, is issued at a discount from its par value and its annual interest expense is implied, but not explicitly paid. The actual interest payment is included in the face value that is paid at maturity. The effects of zero-coupon bonds on the financial statements are qualitatively the same as any discount bond, but the impact is larger because the discount is larger.

Issuance costs :

Issuing a bond involves legal and accounting fees, printing costs, sales commissions, and other fees. Under U.S. GAAP, issuance costs are capitalized as an asset (deferred charge) and allocated to the income statement as an expense over the term of the bond.

Under IFRS, the initial bond liability on the balance sheet is reduced by the amount of issuance costs, increasing the bond’s effective interest rate. In effect, issuance costs are treated as unamortized discount.

Fair value reporting option :

Recall that the book value of a bond liability is based on its market yield at issuance. So, as long as the bond’s yield does not change, the bond liability represents fair (market) value. However, if the yield changes, the balance sheet liability is no longer equal to fair value.

An increase in the bond’s yield will result in a decrease in the fair value of the bond liability. Conversely, a decrease in the bond’s yield increases its fair value. Changes in yield result in a divergence between the book value of the bond liability and the fair value of the bond. The fair value of the bond is the economic liability at a point in time.

IFRS and U.S. GAAP give firms the irrevocable option to report debt at fair value. Under this option, gains (decreases in bond liability) and losses (increases in bond liability) that result from changes in bonds’ market yields are reported in the income statement.

Summary of financial statement effects of issuing a bond :

Cash Flow Impact of issuing a bond :

Income statement impact of issuing a bond :

Interest expense = (market rate at issue) x (balance sheet value of liability)

Interest expense = (market rate at issue) x (balance sheet value of liability)

Balance sheet impact of issuing a bond :

C. Derecognition of debt :

When bonds mature, no gain or loss is recognized by the issuer. At maturity, any original discount or premium has been fully amortized; thus, the book value of a bond liability and its face value are the same. The cash outflow to repay a bond is reported in the cash flow statement as a financing cash flow.

A firm may choose to redeem bonds before maturity because interest rates have fallen, because the firm has generated surplus cash through operations, or because funds from the issuance of equity make it possible.

When bonds are redeemed before maturity, a gain or loss is recognized by subtracting the redemption price from the book value of the bond liability at the reacquisition date.

Under U.S. GAAP, any remaining unamortized bond issuance costs must be written off and included in the gain or loss calculation. Writing off the cost of issuing the bond will reduce a gain or increase a loss. No write-off is necessary under IFRS because the issuance costs are already accounted for in the book value of the bond liability.

Any gain or loss from redeeming debt is reported in the income statement, usually as a part of continuing operations, and additional information is disclosed separately. Redeeming debt is usually not a part of the firm’s day-to-day operations; thus, analysts often eliminate the gain or loss from the income statement for analysis and forecasting.

When presenting the cash flow statement using the indirect method, any gain (loss) is subtracted from (added to) net income in calculating cash flow from operations. The redemption price is reported as an outflow from financing activities.

D. Role of debt covenants in protecting creditors :

Debt covenants are restrictions imposed by the lender on the borrower to protect the lender’s position. Debt covenants can reduce default risk and thus reduce borrowing costs. The restrictions can be in the form of affirmative covenants or negative covenants.

With affirmative covenants, the borrower promises to do certain things, such as :

With negative covenants, the borrower promises to refrain from certain activities that might adversely affect its ability to repay the outstanding debt, such as :

The bondholders can demand immediate repayment of principal if the firm violates a covenant (technical default). Analyzing the covenants is a necessary component of the credit analysis of a bond. Bond covenants are typically discussed in the financial statement footnotes.

E. Financial statement presentation of and disclosures relating to debt :

Firms will often report all of their outstanding long-term debt on a single line on the balance sheet. The portion that is due within the next year is reported as current liability. The firm separately discloses more detail about its long-term debt in the footnotes. They usually include a discussion of :

A discussion of the firm’s long-term debt is also found in the Management Discussion and Analysis section. This discussion is both quantitative and qualitative.

F. Explain the motivations for leasing assets instead of purchasing them :

A lease is a contractual agreement whereby the lessor, the owner of the asset, allows the lessee to use the asset for a specified period of time in return for periodic payments.

Leases are classified as either finance leases or operating leases.

A finance lease is, in substance, a purchase of an asset that is financed with debt. Accordingly, at the inception of the lease, the lessee will add equal amounts to both assets and liabilities on the balance sheet. Over the term of the lease, the lessee will recognize depreciation expense on the asset and interest expense on the liability.

An operating lease is essentially a rental arrangement. No asset or liability is reported by the lessee and the periodic lease payments are simply recognized as rental expenses in the income statement.

Leases can have certain benefits :

G. Difference between a finance lease and an operating lease from the perspectives of the lessor and the lessee :

Lessee’s perspective :

Under IFRS, the classification of a lease is determined by the economic substance of the transaction. If substantially all the rights and risks of ownership are transferred to the lessee, the lease is treated as a finance lease. Circumstances that require a lease to be treated as a finance lease include :

Under U.S. GAAP, the criteria are conceptually similar, but are more specific that under IFRS. A lessee must treat a lease as a capital (finance) lease if any of the following criteria are met :

Lessor’s perspective :

From the lessor’s perspective, the lease is also classified as either an operating lease or a finance (capital) lease.

Under IFRS, classification by the lessor is the same as the lessee’s; that is, if substantially all the rights and risks of ownership are transferred to the lessee, the lease is treated as a finance lease. Otherwise, the lease is treated as an operating lease.

Under U.S. GAAP, if any one of the capital (finance) lease criteria for lessees is met, and the collectability of lease payments is reasonably certain, and the lessor has substantially completed performance, the lessor must treat the lease as capital (finance) lease. Otherwise, the lessor will treat the lease as an operating lease.

With an operating lease, the lessor recognizes rental income and continues to report and depreciate the leased asset on its balance sheet. With a capital (finance) lease, the lessor removes the leased asset from the balance sheet and replaces it with a lease investment account (lease receivable).

H. Initial recognition, initial measurement, and subsequent measurement of finance leases :

Reporting by the lessee :

The treatment of a lease as either an operating lease or finance lease determines whether the lease is reported on the balance sheet, how the lease expense is recognized in the income statement, and the classification of the lease payments on the cash flow statement.

Operating lease. At the inception of the lease, the balance sheet is unaffected. No asset or liability is reported by the lessee. During the term of the lease, rent expense equal to the lease payment is recognized in the lessee’s income statement. In the cash flow statement, the lease payment is reported as an outflow from operating activities.

Finance lease. At the inception of the lease, the lower of the present value of future minimum lease payments or the fair value of the leased asset is recognized as both an asset and as a liability on the lessee’s balance sheet. Over the term of the lease, the asset is depreciated in the income statement and interest expense is recognized. Interest expense is equal to the lease liability at the beginning of the period multiplied by the lease interest rate.

In the cash flow statement, the lease payment is separated into its interest and principal components. Under U.S. GAAP, interest paid is reported in the cash flow statement as an outflow from operating activities and the principal payment is reported as an outflow fro financing activities.

Financial statement and ratio effects of operating and finance leases :

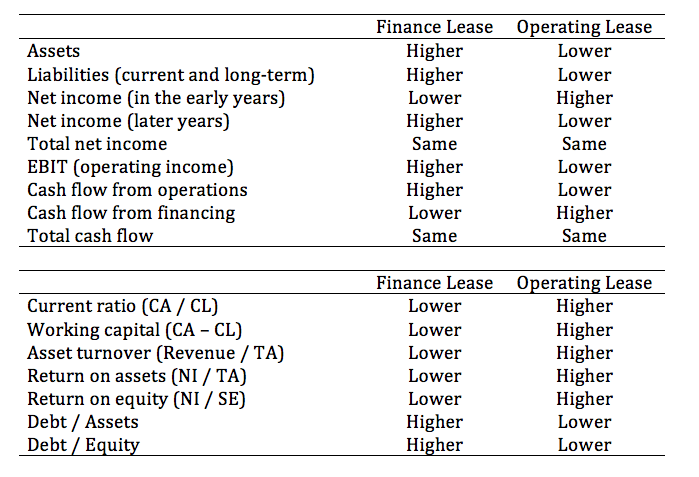

Balance sheet. A finance lease results in a reported asset and liability. Consequently, turnover ratios that use total or fixed assets in their denominators will be lower when a lease is treated as a finance lease as compared to an operating lease. For the same reason, return on assets will also be lower for finance leases. Most importantly, leverage ratios, such as debt-to-assets ratio and the debt-to-equity ratio, will be higher with finance leases than with operating leases because of the reported liability. The principal payment due within the next year is reported as a current liability on the lessee’s balance sheet. This reduces the lessee’s current ratio and working capital.

Because the liability for an operating lease does not appear on the lessee’s balance sheet, operating leases are sometimes referred to as off-balance-sheet financing activities.

Income statement. Operating income (EBIT) will be higher for companies that use finance leases relative to companies that use operating leases. With an operating lease, the entire lease payment is an operating expense, while for a finance lease, only depreciation of the leased asset (not the interest portion) is treated as an operating expense.

Total expense over the life of a lease will be the same whether it is accounted for as an operating lease or a finance (capital) lease because the sum of depreciation expense and interest expense will equal the total of the lease payments. In the early years of a finance lease, however, the interest expense is higher, so the sum of depreciation and interest expense is greater than lease payment. Consequently, net income will be lower for a finance lease in its early years and higher in its later years, compared to an operating lease.

Cash flow statement. Total cash flow is unaffected by the accounting treatment of a lease. However, for a finance lease, cash flow from operations is higher, and cash flow from financing in lower, compared to an operating lease.

The next figures summarize the differences between the effects of finance leases and operating leases on the financial statements and ratios of the lessee :

When bonds mature, no gain or loss is recognized by the issuer. At maturity, any original discount or premium has been fully amortized; thus, the book value of a bond liability and its face value are the same. The cash outflow to repay a bond is reported in the cash flow statement as a financing cash flow.

A firm may choose to redeem bonds before maturity because interest rates have fallen, because the firm has generated surplus cash through operations, or because funds from the issuance of equity make it possible.

When bonds are redeemed before maturity, a gain or loss is recognized by subtracting the redemption price from the book value of the bond liability at the reacquisition date.

Under U.S. GAAP, any remaining unamortized bond issuance costs must be written off and included in the gain or loss calculation. Writing off the cost of issuing the bond will reduce a gain or increase a loss. No write-off is necessary under IFRS because the issuance costs are already accounted for in the book value of the bond liability.

Any gain or loss from redeeming debt is reported in the income statement, usually as a part of continuing operations, and additional information is disclosed separately. Redeeming debt is usually not a part of the firm’s day-to-day operations; thus, analysts often eliminate the gain or loss from the income statement for analysis and forecasting.

When presenting the cash flow statement using the indirect method, any gain (loss) is subtracted from (added to) net income in calculating cash flow from operations. The redemption price is reported as an outflow from financing activities.

D. Role of debt covenants in protecting creditors :

Debt covenants are restrictions imposed by the lender on the borrower to protect the lender’s position. Debt covenants can reduce default risk and thus reduce borrowing costs. The restrictions can be in the form of affirmative covenants or negative covenants.

With affirmative covenants, the borrower promises to do certain things, such as :

- Make timely payments of principal and interest.

- Maintain certain ratios in accordance with specified levels.

- Maintain collateral, if any, in working order.

With negative covenants, the borrower promises to refrain from certain activities that might adversely affect its ability to repay the outstanding debt, such as :

- Increasing dividends or repurchasing shares.

- Issuing more debt.

- Engaging in mergers and acquisitions.

The bondholders can demand immediate repayment of principal if the firm violates a covenant (technical default). Analyzing the covenants is a necessary component of the credit analysis of a bond. Bond covenants are typically discussed in the financial statement footnotes.

E. Financial statement presentation of and disclosures relating to debt :

Firms will often report all of their outstanding long-term debt on a single line on the balance sheet. The portion that is due within the next year is reported as current liability. The firm separately discloses more detail about its long-term debt in the footnotes. They usually include a discussion of :

- The nature of the liabilities.

- Maturity dates.

- Stated and effective interest rates.

- Call provisions and conversion privileges.

- Restrictions imposed by creditors.

- Assets pledged as security.

- The amount of debt maturing in each of the next five years.

A discussion of the firm’s long-term debt is also found in the Management Discussion and Analysis section. This discussion is both quantitative and qualitative.

F. Explain the motivations for leasing assets instead of purchasing them :

A lease is a contractual agreement whereby the lessor, the owner of the asset, allows the lessee to use the asset for a specified period of time in return for periodic payments.

Leases are classified as either finance leases or operating leases.

A finance lease is, in substance, a purchase of an asset that is financed with debt. Accordingly, at the inception of the lease, the lessee will add equal amounts to both assets and liabilities on the balance sheet. Over the term of the lease, the lessee will recognize depreciation expense on the asset and interest expense on the liability.

An operating lease is essentially a rental arrangement. No asset or liability is reported by the lessee and the periodic lease payments are simply recognized as rental expenses in the income statement.

Leases can have certain benefits :

- Less costly financing. Typically, a lease requires no initial down payment. Thus, the lessee conserves cash.

- Reduced risk of obsolescence. At the end of the lease, the asset can be returned to the lessor.

- Less restrictive provisions. Leases can provide more flexibility than other forms of financing because the lease agreement can be negotiated to better suit the needs of each party.

- Off-balance-sheet financing. Entering into an operating lease does not result in a balance sheet liability, so reported leverage ratios are lower compared to borrowing the funds to purchase assets.

- Tax reporting advantages. In the U.S., firms can create a synthetic lease whereby the lease is treated as an ownership position for tax reporting. This allows the lessee to deduct depreciation expense and interest expense for tax purposes.

G. Difference between a finance lease and an operating lease from the perspectives of the lessor and the lessee :

Lessee’s perspective :

Under IFRS, the classification of a lease is determined by the economic substance of the transaction. If substantially all the rights and risks of ownership are transferred to the lessee, the lease is treated as a finance lease. Circumstances that require a lease to be treated as a finance lease include :

- Title to the leased asset is transferred to the lessee at the end of the lease.

- The lessee can purchase the leased asset for a price that is significantly lower than the fair value of the asset at some future date.

- The lease term covers a major portion of the asset’s economic life.

- The present value of the lease payments is substantially equal to the fair value of the leased asset.

- The leased asset is so specialized that only the lessee can use the asset without significant modifications.

Under U.S. GAAP, the criteria are conceptually similar, but are more specific that under IFRS. A lessee must treat a lease as a capital (finance) lease if any of the following criteria are met :

- Title to the leased asset is transferred to the lessee at the end of the lease period.

- A bargain purchase option permits the lessee to purchase the leased asset for a price that is significantly lower than the fair market value of the asset at some future date.

- The lease period is 75% or more of the asset’s economic life.

- The present value of the lease payments is 90% of more of the fair value of the lease asset.

Lessor’s perspective :

From the lessor’s perspective, the lease is also classified as either an operating lease or a finance (capital) lease.

Under IFRS, classification by the lessor is the same as the lessee’s; that is, if substantially all the rights and risks of ownership are transferred to the lessee, the lease is treated as a finance lease. Otherwise, the lease is treated as an operating lease.

Under U.S. GAAP, if any one of the capital (finance) lease criteria for lessees is met, and the collectability of lease payments is reasonably certain, and the lessor has substantially completed performance, the lessor must treat the lease as capital (finance) lease. Otherwise, the lessor will treat the lease as an operating lease.

With an operating lease, the lessor recognizes rental income and continues to report and depreciate the leased asset on its balance sheet. With a capital (finance) lease, the lessor removes the leased asset from the balance sheet and replaces it with a lease investment account (lease receivable).

H. Initial recognition, initial measurement, and subsequent measurement of finance leases :

Reporting by the lessee :

The treatment of a lease as either an operating lease or finance lease determines whether the lease is reported on the balance sheet, how the lease expense is recognized in the income statement, and the classification of the lease payments on the cash flow statement.

Operating lease. At the inception of the lease, the balance sheet is unaffected. No asset or liability is reported by the lessee. During the term of the lease, rent expense equal to the lease payment is recognized in the lessee’s income statement. In the cash flow statement, the lease payment is reported as an outflow from operating activities.

Finance lease. At the inception of the lease, the lower of the present value of future minimum lease payments or the fair value of the leased asset is recognized as both an asset and as a liability on the lessee’s balance sheet. Over the term of the lease, the asset is depreciated in the income statement and interest expense is recognized. Interest expense is equal to the lease liability at the beginning of the period multiplied by the lease interest rate.

In the cash flow statement, the lease payment is separated into its interest and principal components. Under U.S. GAAP, interest paid is reported in the cash flow statement as an outflow from operating activities and the principal payment is reported as an outflow fro financing activities.

Financial statement and ratio effects of operating and finance leases :

Balance sheet. A finance lease results in a reported asset and liability. Consequently, turnover ratios that use total or fixed assets in their denominators will be lower when a lease is treated as a finance lease as compared to an operating lease. For the same reason, return on assets will also be lower for finance leases. Most importantly, leverage ratios, such as debt-to-assets ratio and the debt-to-equity ratio, will be higher with finance leases than with operating leases because of the reported liability. The principal payment due within the next year is reported as a current liability on the lessee’s balance sheet. This reduces the lessee’s current ratio and working capital.

Because the liability for an operating lease does not appear on the lessee’s balance sheet, operating leases are sometimes referred to as off-balance-sheet financing activities.

Income statement. Operating income (EBIT) will be higher for companies that use finance leases relative to companies that use operating leases. With an operating lease, the entire lease payment is an operating expense, while for a finance lease, only depreciation of the leased asset (not the interest portion) is treated as an operating expense.

Total expense over the life of a lease will be the same whether it is accounted for as an operating lease or a finance (capital) lease because the sum of depreciation expense and interest expense will equal the total of the lease payments. In the early years of a finance lease, however, the interest expense is higher, so the sum of depreciation and interest expense is greater than lease payment. Consequently, net income will be lower for a finance lease in its early years and higher in its later years, compared to an operating lease.

Cash flow statement. Total cash flow is unaffected by the accounting treatment of a lease. However, for a finance lease, cash flow from operations is higher, and cash flow from financing in lower, compared to an operating lease.

The next figures summarize the differences between the effects of finance leases and operating leases on the financial statements and ratios of the lessee :

Financial statement and ratio impact of Lease Accounting

In sum, all the ratios in the figure above are worse when lease is capitalized. The only improvements from a finance lease are higher EBIT, higher CFO, and higher net income in the later years of the lease.

Reporting by the Lessor :

From the lessor’s perspective, a capital lease under U.S. GAAP is treated as either a sales-type lease or a direct financing lease. If the present value of the lease payments exceeds the carrying value of the asset, the lease is treated as a sales-type lease. If the present value of the lease payments is equal to the carrying value, the lease is treated as a direct financing lease.

IFRS does not distinguish between a sales-type lease and a direct financing lease. However, similar treatment to a sales-type lease is allowed under IFRS for finance leases originated by manufacturers or dealers.

Sales-type lease :

A sales-type lease is treated as if the lessor sold the asset for the present value of the lease payments and provided a loan to the buyer in the same amount. Sales-type leases are typical when the lessor is a manufacturer or dealer because the cost (balance sheet value) of the leased asset is usually less than its fair value.

At the inception of the lease, the lessor recognizes a sale equal to the present value of the lease payments, and cost of goods sold equal to the carrying value of the asset. Just as with a normal sales transaction, the difference between the sales price and cost of goods sold is gross profit. The asset is removed from the balance sheet and a lease receivable is created, equal to the present value of the lease payments. As the lease payments are received, the principal portion of the payment is recognized as interest income. The interest portion of each lease payment is equal to the lease receivable at the beginning of the period multiplied by the lease interest rate.

In the cash flow statement, the interest portion of the lease payment is reported as an inflow from operating activities, and the principal reduction is reported as an inflow from investing activities, just as with an amortizing loan.

Direct financing lease :

In a direct financing lease, no gross profit is recognized by the lessor at the inception of the lease. Because the present value of the lease payments is equal to the carrying value of leased asset, the lessor is simply providing a financing function to the lessee. In this case, the lessor is not usually a manufacturer or dealer, but has purchased the asset from a third party.

At the inception of the lease, the lessor removes the asset from its balance sheet and creates a lease receivable in the same amount. As the lease payments are received, the principal portion of each payment reduces the lease receivable.

In the income statement, the lessor recognizes interest income over the term of the lease. The interest portion of each lease payment is equal to the lease receivable at the beginning of the period multiplied by the interest rate.

In the cash flow statement, the interest portion is reported as inflow from operating activities and the principal reduction is reported as an inflow from investing activities.

Operating lease :

If the lease is treated as an operating lease, the lessor simply recognizes the lease payment as rental income. In addition, the lessor will keep the leased asset on its balance sheet and depreciate it over its useful life.

I. Disclosures relating to finance and operating leases :

Both lessees and lessors are required to disclose useful information about finance leases and operating leases in the financial statements or in the footnotes, including :

For lessees, analysts often use the disclosures to estimate the off-balance-sheet liabilities of operating leases.

J. Defined contribution and defined benefit pension plans :

A pension is a form of deferred compensation earned over time through employee service. The most common pension arrangements are defined contribution plans and defined benefit plans.

A defined contribution plan is a retirement plan in which the firm contributes a sum each period to the employee’s retirement account. The firm’s contribution can be based on any number of factors, including years of service, the employee’s age, compensation, profitability, or even a percentage of the employee’s contribution. In any event, the firm makes no promise to the employee regarding the future value of the plan assets. The investment decisions are left to the employee, who assumes all of the investment risk.

The financial reporting requirements for defined contribution plans are straightforward. Pension expense is simply equal to the employer’s contribution. There is no future obligation to report on the balance sheet.

In a defined benefit plan, the firm promises to make periodic payments to employees after retirement. The benefit is usually based on the employee’s years of service and the employee’s compensation at, or near, retirement. For example, an employee might earn a retirement benefit of 2% of her final salary year of service. Consequently, an employee with 20 years of service and a final salary of $100,000, would receive $40,000 ($100,000 final salary x 2% x 20 years of service) each year upon retirement until death. Because the employee’s future benefit is defined, the employer assumes the investment risk.

Financial reporting for a defined benefit plan is much more complicated than for a defined contribution plan because the employer must estimate the value of the future obligation to its employees. The obligation involves forecasting a number of variables, such as future compensation levels, employee turnover, retirement age, mortality rates, and an appropriate discount rate.

The present value of the future obligation is known as the defined benefit obligation. Simply stated, the defined benefit obligation is the present value of the amount owed to employees for future pension benefits earned to date.

A company that offers defined pension benefits typically funds the plan by contributing assets to a separate legal entity, usually a trust. The plan assets are managed to generate the income and principal growth necessary to pay the pension benefits as they come due.

For a defined benefit plan, pension expense consists of the following :

IFRS and U.S. GAAP allow firms to smooth the effects of changes in actuarial assumptions and prior service costs over time. Smoothing results is less volatile pension expense.

K. Presentation and disclosure of defined contribution and defined benefit pension plans :

The difference between the defined benefit obligation and the plan assets is referred to as the funded status of the plan. If the value of the plan assets exceeds the present value of the benefit obligation, the plan is said to be overfunded. Conversely, if the benefit obligation exceeds the plan assets, the plan is underfunded. The funded status represents the economic reality of the plan.

Under U.S. GAAP, the funded status is reported on the balance sheet. Thus, an overfunded amount of a pension is reported as an asset and an underfunded amount is reported a liability.

Under IFRS, firms remove unrecognized actuarial gains and losses and unrecognized prior service costs from the funded status. The result is a balance sheet amount that does not represent economic reality.

Under IFRS and U.S. GAAP, firms separately disclose the components of the benefit obligation, plan assets, and pension expense. In addition, firms disclose the assumptions used to calculate pension expense, such as the discount rate, the compensation growth rate, and the expected rate of return on plan assets.

L. Interpret leverage and coverage ratios :

Analysts use solvency ratios to measure a firm’s ability to satisfy its long-term obligations. In evaluating solvency, analysts look at leverage ratios and coverage ratios.

Leverage ratios :

Leverage ratios focus on the balance sheet by measuring the amount of debt in a firm’s capital structure. For calculating these ratios, “debt” refers to interest-bearing obligations. Non-interest bearing liabilities, such as accounts payable, accrued liabilities, and deferred taxes, are not considered debt.

Measures the percentage of total assets financed with debt.

Measures the percentage of total capital financed with debt. Debt-to-capital is similar to the debt-to-assets ratio, except that total capital excludes non-interest bearing liabilities. Recall the balance sheet equation A = L + E. Thus, total assets and total capital differ by the firm’s non-interest bearing liabilities.

Measure of leverage used in the DuPont formula.

All of these leverage ratios are interpreted similarly : that is, the higher the ratio, the higher the leverage. When comparing firms, analysts must remember that in some countries, debt financing is more popular than equity financing. Firms in these countries will have higher leverage.

Coverage ratios :

Coverage ratios focus on the income statement by measuring the sufficiency of earnings to repay interest and other fixed charges when due. Two popular coverage ratios are the interest coverage ratio and the fixed charge coverage ratio.

A firm with lower interest coverage will have more difficulty meeting its interest payments.

Similar to interest coverage ratio but more inclusive because operating lease payments are added to the numerator and denominator. Significant operating lease payments will reduce this ratio as compared to interest coverage. Fixed charge coverage is more meaningful for firms that engage in significant operating leases.

Reporting by the Lessor :

From the lessor’s perspective, a capital lease under U.S. GAAP is treated as either a sales-type lease or a direct financing lease. If the present value of the lease payments exceeds the carrying value of the asset, the lease is treated as a sales-type lease. If the present value of the lease payments is equal to the carrying value, the lease is treated as a direct financing lease.

IFRS does not distinguish between a sales-type lease and a direct financing lease. However, similar treatment to a sales-type lease is allowed under IFRS for finance leases originated by manufacturers or dealers.

Sales-type lease :

A sales-type lease is treated as if the lessor sold the asset for the present value of the lease payments and provided a loan to the buyer in the same amount. Sales-type leases are typical when the lessor is a manufacturer or dealer because the cost (balance sheet value) of the leased asset is usually less than its fair value.

At the inception of the lease, the lessor recognizes a sale equal to the present value of the lease payments, and cost of goods sold equal to the carrying value of the asset. Just as with a normal sales transaction, the difference between the sales price and cost of goods sold is gross profit. The asset is removed from the balance sheet and a lease receivable is created, equal to the present value of the lease payments. As the lease payments are received, the principal portion of the payment is recognized as interest income. The interest portion of each lease payment is equal to the lease receivable at the beginning of the period multiplied by the lease interest rate.

In the cash flow statement, the interest portion of the lease payment is reported as an inflow from operating activities, and the principal reduction is reported as an inflow from investing activities, just as with an amortizing loan.

Direct financing lease :

In a direct financing lease, no gross profit is recognized by the lessor at the inception of the lease. Because the present value of the lease payments is equal to the carrying value of leased asset, the lessor is simply providing a financing function to the lessee. In this case, the lessor is not usually a manufacturer or dealer, but has purchased the asset from a third party.

At the inception of the lease, the lessor removes the asset from its balance sheet and creates a lease receivable in the same amount. As the lease payments are received, the principal portion of each payment reduces the lease receivable.

In the income statement, the lessor recognizes interest income over the term of the lease. The interest portion of each lease payment is equal to the lease receivable at the beginning of the period multiplied by the interest rate.

In the cash flow statement, the interest portion is reported as inflow from operating activities and the principal reduction is reported as an inflow from investing activities.

Operating lease :

If the lease is treated as an operating lease, the lessor simply recognizes the lease payment as rental income. In addition, the lessor will keep the leased asset on its balance sheet and depreciate it over its useful life.

I. Disclosures relating to finance and operating leases :

Both lessees and lessors are required to disclose useful information about finance leases and operating leases in the financial statements or in the footnotes, including :

- General description of the lease arrangement.

- The nature, timing, and amount of payments to be paid or received in each of the next five years. Lease payments after five years can be aggregated.

- Amount of lease revenue and expense reported in the income statement for each period presented.

- Amounts receivable and unearned revenues from lease arrangements.

- Restrictions imposed by lease agreements.

For lessees, analysts often use the disclosures to estimate the off-balance-sheet liabilities of operating leases.

J. Defined contribution and defined benefit pension plans :

A pension is a form of deferred compensation earned over time through employee service. The most common pension arrangements are defined contribution plans and defined benefit plans.

A defined contribution plan is a retirement plan in which the firm contributes a sum each period to the employee’s retirement account. The firm’s contribution can be based on any number of factors, including years of service, the employee’s age, compensation, profitability, or even a percentage of the employee’s contribution. In any event, the firm makes no promise to the employee regarding the future value of the plan assets. The investment decisions are left to the employee, who assumes all of the investment risk.

The financial reporting requirements for defined contribution plans are straightforward. Pension expense is simply equal to the employer’s contribution. There is no future obligation to report on the balance sheet.

In a defined benefit plan, the firm promises to make periodic payments to employees after retirement. The benefit is usually based on the employee’s years of service and the employee’s compensation at, or near, retirement. For example, an employee might earn a retirement benefit of 2% of her final salary year of service. Consequently, an employee with 20 years of service and a final salary of $100,000, would receive $40,000 ($100,000 final salary x 2% x 20 years of service) each year upon retirement until death. Because the employee’s future benefit is defined, the employer assumes the investment risk.

Financial reporting for a defined benefit plan is much more complicated than for a defined contribution plan because the employer must estimate the value of the future obligation to its employees. The obligation involves forecasting a number of variables, such as future compensation levels, employee turnover, retirement age, mortality rates, and an appropriate discount rate.

The present value of the future obligation is known as the defined benefit obligation. Simply stated, the defined benefit obligation is the present value of the amount owed to employees for future pension benefits earned to date.

A company that offers defined pension benefits typically funds the plan by contributing assets to a separate legal entity, usually a trust. The plan assets are managed to generate the income and principal growth necessary to pay the pension benefits as they come due.

For a defined benefit plan, pension expense consists of the following :

- Service cost is the present value of benefits earned by the employees during the current period. Service cost increases the benefit obligation.

- Interest cost is the increase in the benefit obligation due to the passage of time.

- The expected return on plan assets reduces pension expense.

- Actuarial gains and losses are based on assumptions the actuary must make about the benefits to be paid in the future.

- Prior service costs are retroactive benefits awarded to employees when a plan is initiated or amended.

IFRS and U.S. GAAP allow firms to smooth the effects of changes in actuarial assumptions and prior service costs over time. Smoothing results is less volatile pension expense.

K. Presentation and disclosure of defined contribution and defined benefit pension plans :

The difference between the defined benefit obligation and the plan assets is referred to as the funded status of the plan. If the value of the plan assets exceeds the present value of the benefit obligation, the plan is said to be overfunded. Conversely, if the benefit obligation exceeds the plan assets, the plan is underfunded. The funded status represents the economic reality of the plan.

Under U.S. GAAP, the funded status is reported on the balance sheet. Thus, an overfunded amount of a pension is reported as an asset and an underfunded amount is reported a liability.

Under IFRS, firms remove unrecognized actuarial gains and losses and unrecognized prior service costs from the funded status. The result is a balance sheet amount that does not represent economic reality.

Under IFRS and U.S. GAAP, firms separately disclose the components of the benefit obligation, plan assets, and pension expense. In addition, firms disclose the assumptions used to calculate pension expense, such as the discount rate, the compensation growth rate, and the expected rate of return on plan assets.

L. Interpret leverage and coverage ratios :

Analysts use solvency ratios to measure a firm’s ability to satisfy its long-term obligations. In evaluating solvency, analysts look at leverage ratios and coverage ratios.

Leverage ratios :

Leverage ratios focus on the balance sheet by measuring the amount of debt in a firm’s capital structure. For calculating these ratios, “debt” refers to interest-bearing obligations. Non-interest bearing liabilities, such as accounts payable, accrued liabilities, and deferred taxes, are not considered debt.

- Debt-to-assets ratio = total debt/ total assets

Measures the percentage of total assets financed with debt.

- Debt-to-capital ratio = total debt / (total debt + total equity)

Measures the percentage of total capital financed with debt. Debt-to-capital is similar to the debt-to-assets ratio, except that total capital excludes non-interest bearing liabilities. Recall the balance sheet equation A = L + E. Thus, total assets and total capital differ by the firm’s non-interest bearing liabilities.

- Debt-to-equity ratio = total debt / total equity

Measure of leverage used in the DuPont formula.

All of these leverage ratios are interpreted similarly : that is, the higher the ratio, the higher the leverage. When comparing firms, analysts must remember that in some countries, debt financing is more popular than equity financing. Firms in these countries will have higher leverage.

Coverage ratios :

Coverage ratios focus on the income statement by measuring the sufficiency of earnings to repay interest and other fixed charges when due. Two popular coverage ratios are the interest coverage ratio and the fixed charge coverage ratio.

- Interest coverage ratio = EBIT / interest payments.

A firm with lower interest coverage will have more difficulty meeting its interest payments.

- Fixed charge coverage = (EBIT + lease payments) / (interest payments + lease payments)

Similar to interest coverage ratio but more inclusive because operating lease payments are added to the numerator and denominator. Significant operating lease payments will reduce this ratio as compared to interest coverage. Fixed charge coverage is more meaningful for firms that engage in significant operating leases.

Follow this link to next chapter 33. Financial Reporting Quality : Red Flags and Accounting Warning Signs.

Follow this link to Summary.

Follow this link to Summary.

|

|