27. Understanding Cash Flow Statements

A. Cash flow from operating, investing, and financing activities and classification of cash flow items :

Items on the cash flow statement come from two sources :

- Income statement items.

- Changes in balance sheet accounts.

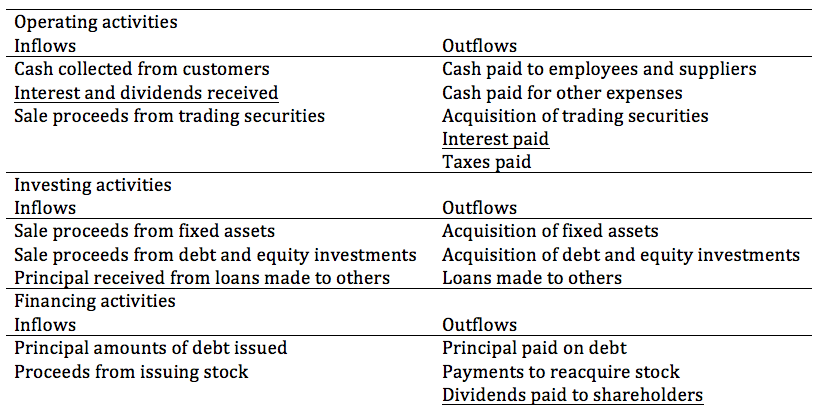

Cash flows are classified in the cash flow statement either as operating, investing, or financing activities.

Cash flow from operating activities (CFO) consists of the inflows and outflows of cash resulting from transactions that affect a firm’s net income.

Cash flow from investing activities (CFI) consists of the inflows and outflows of cash resulting from the acquisition of disposal of long-term assets and certain investments.

Cash flow from financing activities (CFF) consists of the inflows and outflows of cash resulting from transactions affecting a firm’s capital structure.

Examples of each cash flow classification, in accordance with U.S. GAAP, are presented in the following :

B. How non-cash investing and financing activities are reported :

Non-cash investing and financing activities are not reported in the cash flow statement since they do not result in inflows or outflows of cash.

Non-cash transactions must be disclosed in either a footnote or supplemental schedule to the cash flow statement.

C. Differences between IFRS and U.S. GAAP cash flow statements:

IFRS allows more flexibility in the classification of cash flows.

Under IFRS, interest and dividends received may be classified as either operating or investing activities (operating cash flow under U.S. GAAP).

Under IFRS, dividends paid to shareholders may be classified as either operating or financing activities (financing cash flow under U.S. GAAP).

Under IFRS, interest paid on the company’s debt may be classified as either operating or financing activities (operating cash flow under U.S. GAAP).

Under IFRS, income taxes are also reported as operating activities, unless the expense is associated with an investing or financing transaction, then the firm can report the taxes as an investing or financing activity.

D. Direct and indirect methods of presenting cash flow :

There are two methods of presenting the cash flow statement : the direct method and the indirect method. Both methods are permitted under U.S. GAAP and IFRS. The difference between the two methods relates to the presentation of cash flow from operating activities. The presentation of cash flows from investing and financing activities is exactly the same under both methods. Total cash flow from operating activities is exactly the same under both methods, only the presentation methods differ.

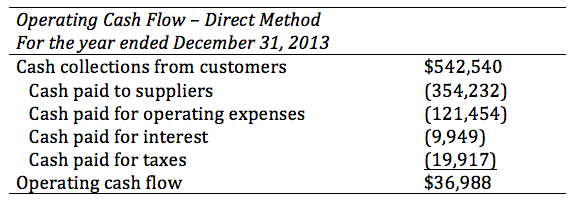

Direct method :

Under the direct method, each line item of the income statement is converted into cash receipts or cash payments. The following contains an example of operating cash flow using the direct method :

Non-cash investing and financing activities are not reported in the cash flow statement since they do not result in inflows or outflows of cash.

Non-cash transactions must be disclosed in either a footnote or supplemental schedule to the cash flow statement.

C. Differences between IFRS and U.S. GAAP cash flow statements:

IFRS allows more flexibility in the classification of cash flows.

Under IFRS, interest and dividends received may be classified as either operating or investing activities (operating cash flow under U.S. GAAP).

Under IFRS, dividends paid to shareholders may be classified as either operating or financing activities (financing cash flow under U.S. GAAP).

Under IFRS, interest paid on the company’s debt may be classified as either operating or financing activities (operating cash flow under U.S. GAAP).

Under IFRS, income taxes are also reported as operating activities, unless the expense is associated with an investing or financing transaction, then the firm can report the taxes as an investing or financing activity.

D. Direct and indirect methods of presenting cash flow :

There are two methods of presenting the cash flow statement : the direct method and the indirect method. Both methods are permitted under U.S. GAAP and IFRS. The difference between the two methods relates to the presentation of cash flow from operating activities. The presentation of cash flows from investing and financing activities is exactly the same under both methods. Total cash flow from operating activities is exactly the same under both methods, only the presentation methods differ.

Direct method :

Under the direct method, each line item of the income statement is converted into cash receipts or cash payments. The following contains an example of operating cash flow using the direct method :

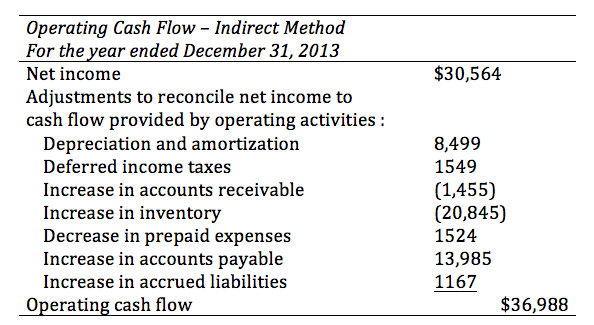

Indirect method :

Under the indirect method, net income is converted to operating cash flow by making adjustments for transactions that affect net income but are not cash transactions. These adjustments include eliminating noncash expenses (depreciation, amortization), non-operating items (gains and losses), and changes in balance sheet accounts resulting from accrual accounting events. The following contains an example of operating cash flow using the indirect method :

Under the indirect method, net income is converted to operating cash flow by making adjustments for transactions that affect net income but are not cash transactions. These adjustments include eliminating noncash expenses (depreciation, amortization), non-operating items (gains and losses), and changes in balance sheet accounts resulting from accrual accounting events. The following contains an example of operating cash flow using the indirect method :

Arguments in favor of each model :

It is the direct method, not the indirect method, that presents operating cash receipts and payments and is this more consistent with the objectives of the cash flow statement. The direct method provides more information that the indirect method and is preferred by analysts who are estimating future cash flows.

The main advantage of the indirect method is that it focuses on the differences in net income and operating cash flow.

Disclosure requirements :

Under U.S. GAAP, a direct method must also disclose the adjustments necessary to reconcile net income to cash flow from operating activities. This reconciliation is not required under IFRS.

Under IFRS, payments for interest and taxes must be disclosed separately in the cash flow statement under either method. Under the U.S. GAAP, payments for interest and taxes can be reported in the cash flow statement or disclosed in the footnotes.

E. How the cash flow statement is linked to the income statement and the balance sheet :

The cash flow statement reconciles the beginning and ending balances of cash over an accounting period. The change in cash is a result of the firm’s operating, investing, and financing activities as follows :

Operating cash flow

+ Investing cash flow

+ Financing cash flow

= Change in cash balance

+ Beginning cash balance

= Ending cash balance

With a few exceptions, operating activities related to the firm’s current assets and current liabilities. Investing activities related to the firm’s non-current assets, and financing activities typically related to the firm’s non-current liabilities and equity.

It is helpful to understand how transactions affect each balance sheet account. For example, accounts receivable are increased by sales and decreased by cash collections. We can summarize as follows :

Beginning accounts receivable

+ Sales

- Cash collections

= Ending accounts receivable

F. Steps in the preparation of direct and indirect cash flow statements, including how cash flows can be computed using income statement and balance sheet data :

Cash Flow from Investing activities :

CFI are calculated by examining the change in the gross asset accounts that result from investing activities, such as PP&E, intangible assets, and investment securities. Related accumulated depreciation or amortization accounts are ignored since they do not represent cash expenses.

When calculating cash paid for a new asset, it is necessary to determine whether old assets were sold. The following formula must be used :

beginning gross assets + cash paid for new assets – gross cost of assets sold = ending gross assets

When calculating the cash flow from an asset that has been sold, it is necessary to consider any gain or loss from the sale using the following :

cash from asset sold = book value of the asset + gain (or – loss) on sale

Cash Flow from Financing activities :

CFF are determined by measuring the cash flows occurring between the firm and suppliers of capital.

Cash flows between the firm and its creditors result from new borrowings (positive CFF) and debt principal repayments (negative CFF). Cash flows between the firm and its shareholders occur when equity is issued, shares are repurchased, or dividends are paid. CFF is the sum of these two measures :

net cash flows from creditors = new borrowings – principal amounts repaid

net cash flows from shareholders = new equity issued – share repurchases – cash dividends paid

Cash dividends paid can be calculated from dividends declared and any changes in dividends payable :

beginning dividends payable + dividends declared – dividends paid = ending dividends payable

If the dividends declared amount is not provided, it can be calculated using :

beginning retained earnings + net income – ending retained earnings = ending retained earnings

Cash Flow from Operating Activities :

Direct method :

The direct method of presenting a firm’s statement of cash flows shows only cash payments and cash receipts over the period. The sum of these inflows and outflows is the company’s CFO.

The following are common components of cash flow that appear on a statement of cash flow presented under the direct method:

Indirect method :

The steps in calculating CFO under the indirect method can be summarized as follows :

Step 1 : Begin with net income.

Step 2 : Subtract gains or add losses that resulted from financing or investing cash flows (such as gains from the sale of land).

Step 3 : Add back all non-cash charges to income (such as depreciation and amortization) and subtract all non-cash components of revenue.

Step 4 : Add or subtract changes to balance sheet operating accounts as follows :

G. Convert cash flows from the indirect to the direct method :

The only difference between the indirect and direct methods of presentation is in the CFO section. CFO under the direct method can be computed using a combination of the income statement and a statement of cash flows prepared under the indirect method or a balance sheet.

There are two major sections in CFO under the direct method : cash inflows (receipts) and cash outflows (payments). We will illustrate the conversion process using some frequently used accounts (not exhaustive). The general principle is to adjust each income statement item for its corresponding balance sheet accounts and to eliminate non-cash and non-operating items.

Cash collections from customers :

Step 1 : Begin with net sales from the income statement.

Step 2 : Subtract (add) any increase (decrease) in the accounts receivable balance as reported in the indirect method. If the company has sold more on credit than has been collected from customers, accounts receivable will increase and cash collections will be less than net sales.

Step 3 : Add (subtract) an increase (decrease) in unearned revenue. Unearned revenue includes cash advances from customers. Cash received from customers when the goods or services have yet to be delivered is not included in net sales, so the advances must be added to net sales in order to calculate cash collections.

Cash payments to suppliers :

Step 1 : Begin with COGS as reported in the income statement.

Step 2 : If depreciation and/or amortization have been included in COGS (they increase COGS), these non-cash expenses must be added back.

Step 3 : Reduce (increase) COGS by any increase (decrease) in the accounts payable balance as reported in the indirect method. If payables have increased, then more was spent on credit purchases during the period than was paid on existing payables, so cash payments are reduced bt the amount of the amount of the increase in payables.

Step 4 : Add (subtract) any increase (decrease) in the inventory balance as disclosed in the indirect method. Increases in inventory are not included in COGS for the period but still represent the purchase of inputs, so they increase cash paid to suppliers.

Step 5 : Subtract an inventory write-off that occurred during the period. An inventory write-off, as a result of applying the lower of cost or market value, will reduce ending inventory and increase COGS for the period. However, no cash flow is associated with the write-off.

Other items in a direct method cash flow statement follow the same principles. Cash taxes (wages, interest) paid, for example, can be derived by starting with income tax (wages, interest) expense on the income statement. Adjustment must be made for changes in related balance sheet accounts (deferred tax assets and liabilities, and income taxes payable).

H. Analysis and interpretation of both reported and common-size cash flow statements :

An analyst should determine whether a company is generating positive operating cash flow over time that is greater than its capital spending needs and whether the company’s accounting policies are causing reported earnings to diverge from operating cash flow.

A common-size cash flow statement shows each item as a percentage of revenues or shows each cash inflow as a percentage of total inflows and each outflow as a percentage of total outflows.

I. Free cash flow to the firm, free cash flow to equity, and performance and coverage cash flow ratios :

Free cash flow is a measure of cash that is available for discretionary purposes. This is the cash flow that is available once the firm has covered its capital expenditures. This is a fundamental cash flow measure and is often used for valuation.

Free Cash Flow to the Firm :

Free cash flow to the firm (FCFF) is the cash available to all investors, both equity owners and debt holders. FCFF can be calculated by starting with either net income or operating cash flow.

FCFF = NI + NCC + (Int x (1 – tax rate)) – FCInv – WCInv

where :

NI = net income

NCC = non-cash charges (depreciation and amortization)

Int = Interest expense

FCInv = fixed capital investment (net capital expenditures)

WCInv = working capital investment

Interest expense, net of tax, is added back to net income. This is because FCFF is the cash flow available to stockholders and debt holders. Since interest is paid to (and therefore ‘available’ to) the debt holders, it must be included in FCFF.

FCFF can also be calculated from operating cash flow as :

FCFF = CFO + (Int x (1 – tax rate)) – FCInv

where :

CFO = cash flow from operations

Int = interest expense

FCInv = fixes capital investment (net capital expenditures)

Free Cash Flow to Equity :

Free cash flow to equity (FCFE) is the cash flow that would be available for distributions to common shareholders. FCFE can be calculated as follows :

FCFE = CFO – FCInv + net borrowing

where :

CFO = cash flow from operations

FCInv = fixed capital investment (net capital expenditures)

net borrowing = debt issued – debt repaid

Other Cash Flow Ratios :

Performance ratios :

The cash flow-to-revenue ratio measures the amount of operating cash flow generated for each dollar of revenue.

cash flow-to-revenue = CFO / net revenue

The cash return-on-assets ratio measures the return of operating cash flow attributed to all providers of capital.

cash return-on-assets = CFO / average total assets

The cash return-on-equity ratio measures the return of operating cash flow attributed to share holders.

cash return-on-equity = CFO / average total equity

The cash-to-income ratio measures the ability to generate cash from firm operations.

cash-to-income = CFO / operating income

Cash flow per share is a variation of the basic earnings per share measured by using CFO instead of net income.

cash flow per share = (CFO – preferred dividends)/ (weighted average number of common shares)

Coverage ratios :

The debt coverage ratio measures financial risk and leverage.

debt coverage = CFO / total debt

The interest coverage ratio measures the firm’s ability to meet its interest obligations :

interest coverage = (CFO + interest paid + taxes paid) / interest paid

The reinvestment ratio measures the firm’s ability to acquire long-term debt with operating cash flow.

reinvestment = CFO / cash paid for long-term assets

The debt payment ratio measures the firm’s ability to satisfy long-term debt with operating cash flow.

debt payment = CFO / cash long-term debt repayment

The dividend payment ratio measures the firm’s ability to make dividend payments from operating cash flow.

dividend payment = CFO / dividends paid

The investing and financing ratio measures the firm’s ability to purchase assets , satisfy debt, and pay dividends.

investing and financing = CFO / cash outflows from investing and financing activities

It is the direct method, not the indirect method, that presents operating cash receipts and payments and is this more consistent with the objectives of the cash flow statement. The direct method provides more information that the indirect method and is preferred by analysts who are estimating future cash flows.

The main advantage of the indirect method is that it focuses on the differences in net income and operating cash flow.

Disclosure requirements :

Under U.S. GAAP, a direct method must also disclose the adjustments necessary to reconcile net income to cash flow from operating activities. This reconciliation is not required under IFRS.

Under IFRS, payments for interest and taxes must be disclosed separately in the cash flow statement under either method. Under the U.S. GAAP, payments for interest and taxes can be reported in the cash flow statement or disclosed in the footnotes.

E. How the cash flow statement is linked to the income statement and the balance sheet :

The cash flow statement reconciles the beginning and ending balances of cash over an accounting period. The change in cash is a result of the firm’s operating, investing, and financing activities as follows :

Operating cash flow

+ Investing cash flow

+ Financing cash flow

= Change in cash balance

+ Beginning cash balance

= Ending cash balance

With a few exceptions, operating activities related to the firm’s current assets and current liabilities. Investing activities related to the firm’s non-current assets, and financing activities typically related to the firm’s non-current liabilities and equity.

It is helpful to understand how transactions affect each balance sheet account. For example, accounts receivable are increased by sales and decreased by cash collections. We can summarize as follows :

Beginning accounts receivable

+ Sales

- Cash collections

= Ending accounts receivable

F. Steps in the preparation of direct and indirect cash flow statements, including how cash flows can be computed using income statement and balance sheet data :

Cash Flow from Investing activities :

CFI are calculated by examining the change in the gross asset accounts that result from investing activities, such as PP&E, intangible assets, and investment securities. Related accumulated depreciation or amortization accounts are ignored since they do not represent cash expenses.

When calculating cash paid for a new asset, it is necessary to determine whether old assets were sold. The following formula must be used :

beginning gross assets + cash paid for new assets – gross cost of assets sold = ending gross assets

When calculating the cash flow from an asset that has been sold, it is necessary to consider any gain or loss from the sale using the following :

cash from asset sold = book value of the asset + gain (or – loss) on sale

Cash Flow from Financing activities :

CFF are determined by measuring the cash flows occurring between the firm and suppliers of capital.

Cash flows between the firm and its creditors result from new borrowings (positive CFF) and debt principal repayments (negative CFF). Cash flows between the firm and its shareholders occur when equity is issued, shares are repurchased, or dividends are paid. CFF is the sum of these two measures :

net cash flows from creditors = new borrowings – principal amounts repaid

net cash flows from shareholders = new equity issued – share repurchases – cash dividends paid

Cash dividends paid can be calculated from dividends declared and any changes in dividends payable :

beginning dividends payable + dividends declared – dividends paid = ending dividends payable

If the dividends declared amount is not provided, it can be calculated using :

beginning retained earnings + net income – ending retained earnings = ending retained earnings

Cash Flow from Operating Activities :

Direct method :

The direct method of presenting a firm’s statement of cash flows shows only cash payments and cash receipts over the period. The sum of these inflows and outflows is the company’s CFO.

The following are common components of cash flow that appear on a statement of cash flow presented under the direct method:

- Cash collected from customers, typically the main components of CFO.

- Cash used in the production of goods and services (cash inputs).

- Cash operating expenses.

- Cash paid for interest.

- Cash paid for taxes.

Indirect method :

The steps in calculating CFO under the indirect method can be summarized as follows :

Step 1 : Begin with net income.

Step 2 : Subtract gains or add losses that resulted from financing or investing cash flows (such as gains from the sale of land).

Step 3 : Add back all non-cash charges to income (such as depreciation and amortization) and subtract all non-cash components of revenue.

Step 4 : Add or subtract changes to balance sheet operating accounts as follows :

- Increases in the operating asset accounts (uses of cash) are subtracted, while decreases (sources of cash) are added.

- Increases in the operating liability accounts (sources of cash) are added, while decreases (uses of cash) are subtracted.

G. Convert cash flows from the indirect to the direct method :

The only difference between the indirect and direct methods of presentation is in the CFO section. CFO under the direct method can be computed using a combination of the income statement and a statement of cash flows prepared under the indirect method or a balance sheet.

There are two major sections in CFO under the direct method : cash inflows (receipts) and cash outflows (payments). We will illustrate the conversion process using some frequently used accounts (not exhaustive). The general principle is to adjust each income statement item for its corresponding balance sheet accounts and to eliminate non-cash and non-operating items.

Cash collections from customers :

Step 1 : Begin with net sales from the income statement.

Step 2 : Subtract (add) any increase (decrease) in the accounts receivable balance as reported in the indirect method. If the company has sold more on credit than has been collected from customers, accounts receivable will increase and cash collections will be less than net sales.

Step 3 : Add (subtract) an increase (decrease) in unearned revenue. Unearned revenue includes cash advances from customers. Cash received from customers when the goods or services have yet to be delivered is not included in net sales, so the advances must be added to net sales in order to calculate cash collections.

Cash payments to suppliers :

Step 1 : Begin with COGS as reported in the income statement.

Step 2 : If depreciation and/or amortization have been included in COGS (they increase COGS), these non-cash expenses must be added back.

Step 3 : Reduce (increase) COGS by any increase (decrease) in the accounts payable balance as reported in the indirect method. If payables have increased, then more was spent on credit purchases during the period than was paid on existing payables, so cash payments are reduced bt the amount of the amount of the increase in payables.

Step 4 : Add (subtract) any increase (decrease) in the inventory balance as disclosed in the indirect method. Increases in inventory are not included in COGS for the period but still represent the purchase of inputs, so they increase cash paid to suppliers.

Step 5 : Subtract an inventory write-off that occurred during the period. An inventory write-off, as a result of applying the lower of cost or market value, will reduce ending inventory and increase COGS for the period. However, no cash flow is associated with the write-off.

Other items in a direct method cash flow statement follow the same principles. Cash taxes (wages, interest) paid, for example, can be derived by starting with income tax (wages, interest) expense on the income statement. Adjustment must be made for changes in related balance sheet accounts (deferred tax assets and liabilities, and income taxes payable).

H. Analysis and interpretation of both reported and common-size cash flow statements :

An analyst should determine whether a company is generating positive operating cash flow over time that is greater than its capital spending needs and whether the company’s accounting policies are causing reported earnings to diverge from operating cash flow.

A common-size cash flow statement shows each item as a percentage of revenues or shows each cash inflow as a percentage of total inflows and each outflow as a percentage of total outflows.

I. Free cash flow to the firm, free cash flow to equity, and performance and coverage cash flow ratios :

Free cash flow is a measure of cash that is available for discretionary purposes. This is the cash flow that is available once the firm has covered its capital expenditures. This is a fundamental cash flow measure and is often used for valuation.

Free Cash Flow to the Firm :

Free cash flow to the firm (FCFF) is the cash available to all investors, both equity owners and debt holders. FCFF can be calculated by starting with either net income or operating cash flow.

FCFF = NI + NCC + (Int x (1 – tax rate)) – FCInv – WCInv

where :

NI = net income

NCC = non-cash charges (depreciation and amortization)

Int = Interest expense

FCInv = fixed capital investment (net capital expenditures)

WCInv = working capital investment

Interest expense, net of tax, is added back to net income. This is because FCFF is the cash flow available to stockholders and debt holders. Since interest is paid to (and therefore ‘available’ to) the debt holders, it must be included in FCFF.

FCFF can also be calculated from operating cash flow as :

FCFF = CFO + (Int x (1 – tax rate)) – FCInv

where :

CFO = cash flow from operations

Int = interest expense

FCInv = fixes capital investment (net capital expenditures)

Free Cash Flow to Equity :

Free cash flow to equity (FCFE) is the cash flow that would be available for distributions to common shareholders. FCFE can be calculated as follows :

FCFE = CFO – FCInv + net borrowing

where :

CFO = cash flow from operations

FCInv = fixed capital investment (net capital expenditures)

net borrowing = debt issued – debt repaid

Other Cash Flow Ratios :

Performance ratios :

The cash flow-to-revenue ratio measures the amount of operating cash flow generated for each dollar of revenue.

cash flow-to-revenue = CFO / net revenue

The cash return-on-assets ratio measures the return of operating cash flow attributed to all providers of capital.

cash return-on-assets = CFO / average total assets

The cash return-on-equity ratio measures the return of operating cash flow attributed to share holders.

cash return-on-equity = CFO / average total equity

The cash-to-income ratio measures the ability to generate cash from firm operations.

cash-to-income = CFO / operating income

Cash flow per share is a variation of the basic earnings per share measured by using CFO instead of net income.

cash flow per share = (CFO – preferred dividends)/ (weighted average number of common shares)

Coverage ratios :

The debt coverage ratio measures financial risk and leverage.

debt coverage = CFO / total debt

The interest coverage ratio measures the firm’s ability to meet its interest obligations :

interest coverage = (CFO + interest paid + taxes paid) / interest paid

The reinvestment ratio measures the firm’s ability to acquire long-term debt with operating cash flow.

reinvestment = CFO / cash paid for long-term assets

The debt payment ratio measures the firm’s ability to satisfy long-term debt with operating cash flow.

debt payment = CFO / cash long-term debt repayment

The dividend payment ratio measures the firm’s ability to make dividend payments from operating cash flow.

dividend payment = CFO / dividends paid

The investing and financing ratio measures the firm’s ability to purchase assets , satisfy debt, and pay dividends.

investing and financing = CFO / cash outflows from investing and financing activities

|

|