26. Understanding Balance Sheets

A. Three elements of the balance sheet: Assets, Liabilities, and Equity :

The balance sheet (also known as the statement of financial position or statement of financial condition) reports the firm’s financial position at a point in time.

Assets: Resources controlled as a result of past transactions that are expected to provide future economic benefits.

Liabilities: Obligations as a result of past events that are expected to require an outflow of economic resources.

Equity: The owner’s residual interest in the assets after deducting the liabilities. Equity is also referred to as stockholders’ equity, shareholders’ equity, or owners’ equity. It is also referred to as ‘net assets’.

A financial statement item should be recognized if a future economic benefit firm the item (flowing to or from the firm) is probable and item’s value or cost can be measured reliably.

B. Uses and limitations of the balance sheet in financial analysis :

The balance sheet can be used to assess a firm’s liquidity, solvency and ability to make distributions to shareholders.

Balance sheet elements (assets, liabilities, equity) should not be interpreted as market value or intrinsic value. For most firms, the balance sheet consists of a mixture of values. Even if the balance sheet was reported at fair value, the value may have changed since the balance sheet date. Besides, there are a number of assets and liabilities that do not appear on the balance sheet but certainly have value (firm’s employees, reputation...).

C. Alternative formats of balance sheets presentation :

Under U.S. GAAP and IFRS, firms are required to separately report their current assets and non-current assets and current and non-current liabilities. The current/non-current format is known as a classified balance sheet.

Under IFRS, firms can chose to use a liquidity-based format, where assets and liabilities are presented in the order of liquidity (often used in the banking industry), if the presentation is more relevant and reliable.

D. Current and non-current assets, current and non current liabilities :

Current assets: Cash and other assets that will likely be converted into cash or used up within one year or one operating cycle, whichever comes first. Current assets are usually presented in the order of their liquidity, with cash being the most liquid.

Current liabilities: Obligations that will be satisfied within one year or one operating cycle, whichever is greater. More specifically, a liability that meets one of the following criteria is considered current :

- Settlement is expected during the normal operating cycle.

- Settlement is expected within one year.

- Held primarily for trading purposes.

- There is not an unconditional right to defer settlement for more than one year.

Current assets minus current liabilities equals working capital.

Non-current assets: They do not meet the definition of current assets because they will not be converted into cash or used up within one year or operating cycle. They provide information about the firm’s investing activities.

Non-current liabilities: They do not meet the definition of current liabilities. They provide information about the firm’s long-term financing activities.

E. Different types of assets and liabilities and their measurement bases :

- Current asset :

Cash and cash equivalents: Cash equivalents are short-term, highly liquid investments that are readily convertible to cash and near enough to maturity that interest rate risk is insignificant. Examples include Treasury bills, commercial paper, and money market funds. They are reported at amortized cost or fair value, both resulting in about the same value.

Marketable securities: Traded in a public market and whose value can be readily determined. Examples include Treasury bills, notes, bonds, and equity securities. Details of the investment are disclosed in the financial footnotes.

Accounts receivable: They are financial assets that represent amounts owed to the firm by customers for goods or services sold on credit. They are reported at net realizable value, which is based on estimated bad debt expense. Bad debt expense increases the allowance for doubtful accounts, a contra-asset account. Thus, gross receivables less the allowance for doubtful accounts is equal to accounts receivable at net realizable value, the amount the firm expects to collect.

Inventories: Inventories are goods held for sale to customers or used in manufacture of goods to be sold. Manufacturing firms report inventories of raw materials, work-in-process, and finished goods.

Inventories are valued on the balance sheet at the lower of cost or net realizable value.

Other current assets: Other current assets are amounts that may not be material if shown separately; thus, the items are combined into a single amount. Examples include prepaid expenses and deferred tax assets.

Prepaid expenses are operating costs that have been paid in advance.

Deferred tax assets are created when the amount of taxes payable exceeds the amount of income tax expense recognized in the income statement.

- Current liabilities :

Accounts payable: They are amounts the firm owes to suppliers for goods or services purchased on credit.

Notes payable and current portion of long-term debt: Notes payable are obligations in the form of promissory notes owed to creditors and lenders. Notes payables can also be reported as non-current liabilities if their maturities exceed one year. The current portion of long-term debt is the principal portion if debt due within one year or operating cycle, whichever is greater.

Accrued liabilities (expenses): Expenses that have been recognized in the income statement but are not yet contractually due. Accrued liabilities result from the accrual method of accounting, under which expenses are recognized as incurred.

Unearned revenue (deferred revenue, income): Cash collected in advance of providing goods and services.

- Non-current assets :

Property, Plant & Equipment (PP&E): PP&E are tangible assets used in the production of goods and services. PP&E includes land and buildings, machinery and equipment, furniture, and natural resources. Under IFRS, PP&E can be reported using the cost model or the revaluation model. Under U.S. GAAP, only the cost model is allowed.

Under the cost model, PP&E is reported under amortized cost (historical cost minus accumulated depreciation, amortization, depletion, and impairment losses). Historical cost includes the purchase price plus any cost necessary to get the asset ready for use, such as delivery and installation costs. PP&E must be tested for impairment.

Under the revaluation model, PP&E is reported at fair value less any accumulated depreciation. Changes in fair value are reflected in shareholders’ equity and may be recognized in the income statement in certain circumstances.

Investment property: Under IFRS, investment property includes assets that generate rental income or capital appreciation. U.S. GAAP does not have a specific definition of investment property. Under IFRS, investment property can either be reported at amortized cost or fair value. Under the fair value model, any change in fair value is recognized in the income statement.

Intangible assets: Intangible assets are non-monetary assets that lack physical substance. Identifiable intangible assets can be acquired separately or are the result of rights or privileges conveyed to their owner (patents, trademarks, copyrights). Unidentifiable intangible assets cannot be acquired separately and may have an unlimited life (goodwill).

Under IFRS, identifiable intangibles that are purchased can be reported on the balance sheet using the cost model or the revaluation model. Both models are basically the same as the measurement models used for PP&E. Under U.S. GAAP, only the cost model is allowed.

Except for certain legal costs, intangibles that are created internally, such as research and development costs, are expensed as incurred under U.S. GAAP. Under IFRS, a firm must identify the research stage and the development stage. Under IFRS, the firm must expense costs incurred during the research stage but can capitalize costs incurred during the development stage.

Finite-lived assets are amortized over their useful lives and tested for impairment in the same way as PP&E. The amortization method and useful life estimates are reviewed at least annually. Intangible assets with infinite lives are not amortized, but are tested for impairment at least annually.

Under IFRS and U.S. GAAP, all of the following should be expensed as incurred :

- Start-up and training costs.

- Administrative overhead.

- Advertising and promotion costs.

- Relocation and reorganization costs.

- Termination costs.

Goodwill: Goodwill is the excess of purchase price over the fair value of the identifiable net assets acquired in a business acquisition

Goodwill is only created in a purchase acquisition. Internally generated goodwill is expensed as incurred.

Financial assets: Financial instruments are contracts that give rise to both a financial asset of one entity and a financial liability or equity instrument of another entity. Financial assets include investment securities, derivatives, loans, and receivables.

Financial instruments are measured at historical cost, amortized cost, or fair value. Financial assets measured at historical cost (at cost) include equity investments and loans to and receivables from other entities.

Financial assets measured at amortized cost are known as held-to-maturity securities. Held-to-maturity securities are debt securities acquired with the intent to be held to maturity. Amortized cost is equal to the original issue price minus any principal payments, minus any amortized premium, plus any amortized discount, minus any impairment losses.

Financial assets measured at fair value (mark-to-market accounting) include trading securities, available-for-sale securities, and derivatives:

Trading (held-for-trading) securities are debt and equity securities acquired with the intent to profit over the near term. Trading securities are reported on the balance sheet at fair value, and the unrealized gains and losses are recognized in the income statement. Derivative instruments are treated the same as trading securities.

Available-for-sale securities are debt and equity securities that are not expected to be held to maturity in the near term. Like trading securities, available-for-sale securities are reported on the balance sheet at fair value. However, any unrealized gains and losses are recognized in the income statement, but are reported in other comprehensive income as a part of shareholders’ equity.

- Non-current liabilities :

Long-term financial liabilities: Include bank loans, notes payable, bonds payable, and derivatives. If the financial liabilities are not issued at face amount, they are usually reported on the balance sheet at amortized cost. Amortized cost is equal to the issue price minus any principal payments, plus any amortized discount or minus any amortized premium.

Deferred tax liabilities: Amounts of income taxes payable in future periods as a result of taxable temporary differences. They are created when the amount of income tax expense recognized in the income statement is greater than taxes payable.

F. Components of shareholders’ equity :

Owner’s equity: Residual interest in assets that remains after subtracting en entity’s liabilities. Owner’s equity includes contributed capital, preferred stock, treasury stock, retained earnings, non-controlling interest, and accumulated other comprehensive income.

Contributed capital: The amount contributed by the common shareholders. The par value of common stock is a stated or legal value. Par value is the stated or nominal value assigned to the stock. Par value has no relationship with fair value. Some common shares are even issued without a par value. When par value exists, it is reported separately in stockholders’ equity. The amount the firm received from the issuance of common stock is equal to the par value plus the additional paid-in-capital.

Authorized shares are the number of shares that may be sold under the firm’s articles of incorporation. Issued shares are the number of shares that have been actually sold to shareholders. The number of outstanding shares is equal to the issued shares less treasury stock.

Preferred stock: It has certain privileges not conferred by common stock (specific rate paid dividends, priority in the event of liquidation...).

Noncontrolling interest (minority interest) is the minority shareholders’ pro-rata share of the net assets (equity) of a subsidiary that is not wholly owned by the parent.

Retained earnings: Undistributed earnings (net income) of the firm since inception, the cumulative earnings that have not been paid out to shareholders as dividends.

Treasury stock: Stock that has been reacquired by the issuing firm but not yet retired. Has no voting rights and does not receive dividends.

Accumulated other comprehensive income: Include all changes in stockholders’ equity except for transactions recognized in the income statement (net income) and transactions with shareholders, such as issuing stock, reacquiring stock, and paying dividends.

G. Balance sheet and statement of changes in equity analysis :

The balance sheet reports the economic resources and obligations of the firm. Thus, the balance sheet can be used to analyze a firm’s capital structure and ability to repay its short-term obligations.

The statement of changes in stockholders’ equity summarizes all transactions that increase or decrease the equity accounts for the period. The statement includes transactions with shareholders and reconciles the beginning and ending balance of each equity account. In addition, the components of accumulated other comprehensive income are disclosed.

H. Convert balance sheets to common-size balance sheets :

A vertical common-size balance sheet expresses each item of the balance sheet as a percentage of total assets. The common-size format standardizes the balance sheet by eliminating the effects of size. This allows for comparison over time (time-series analysis) and across firms (cross-sectional analysis).

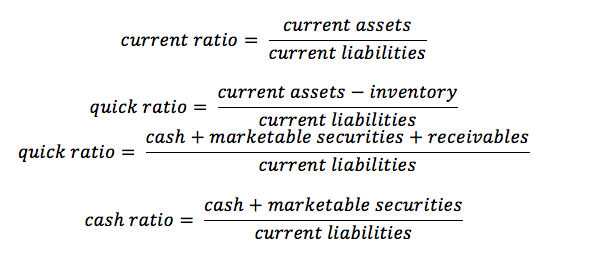

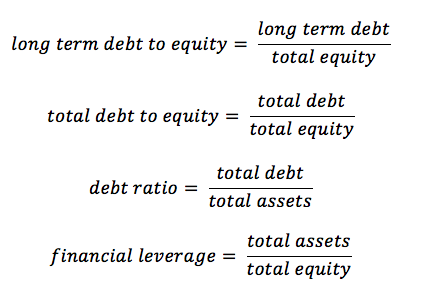

I. Liquidity and solvency ratios :

Liquidity ratios : They measure the firm’s ability to satisfy its short-term obligations as they come due.

Solvency ratios : They measure the firm’s ability to satisfy its long-ter obligations.

Follow this link to next chapter 27. Understanding Cash Flow Statements.

Follow this link to Summary.

Follow this link to Summary.

|

|