6. DISCOUNTED CASH FLOWS APPLICATIONS

A. Calculate and interpret the net present value (NPV) and the internal rate of return (IRR) of an investment :

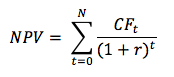

The net present value (NPV) of an investment project is the present value of expected cash inflows associated with the project less the present value of the project’s expected cash outflows, discounted at the appropriate cost of capital. Mathematically, the NPV is expressed as :

where :

CFt = the expected net cash flow at time t

N = the estimated life of the investment

r = the discount rate (opportunity cost of capital)

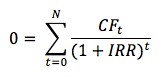

The internal rate of return (IRR) is defined as the rate of return that equates the PV of an investment’s expected benefits (inflows) with the PV of its costs (outflows). The IRR may be defined as the discount rate for which the NPV of an investment is zero. The general formula for the IRR is :

The net present value (NPV) of an investment project is the present value of expected cash inflows associated with the project less the present value of the project’s expected cash outflows, discounted at the appropriate cost of capital. Mathematically, the NPV is expressed as :

where :

CFt = the expected net cash flow at time t

N = the estimated life of the investment

r = the discount rate (opportunity cost of capital)

The internal rate of return (IRR) is defined as the rate of return that equates the PV of an investment’s expected benefits (inflows) with the PV of its costs (outflows). The IRR may be defined as the discount rate for which the NPV of an investment is zero. The general formula for the IRR is :

B. Contrast the NPV rule to the IRR rule, and identify problems associated with the IRR rule :

NPV decision rule : The basic idea behind NPV analysis is that if a project has a positive NPV, this amount goes to the firm’s shareholders. As such, if a firm undertakes a project with a positive NPV, shareholder wealth is increased. The NPV decision rules are summarized :

IRR decision rule : The following are decision rules of IRR analysis :

Note that for a single project, the IRR and NPV rules lead to the same accept/reject decision.

Problems associated with the IRR method

When the acceptance or rejection of one project has no effect on the acceptance or rejection of another, the two projects are considered to be independent projects.

When only one of two projects may be accepted, the projects are considered to be mutually exclusive. For mutually exclusive projects, the NPV and IRR methods can give conflicting project rankings. Given that shareholder wealth maximization is the ultimate goal of the firm, always select the project with the greatest NPV when the IRR and NPV rules provide conflicting results.

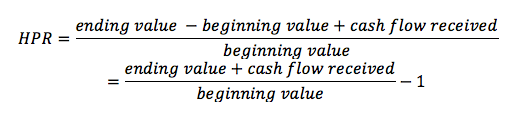

C. Calculate and interpret a holding period return :

A holding period can be any period of time. The holding period return (HPR) is simply the percentage change in the value of an investment over the period it is held. If the asset has cash flows, such as dividend or interest payments, we refer to the return as the total return.

D. Calculate and compare the money-weighted and time-weighted rates of return of a portfolio and evaluate the performance of portfolios based on these measures :

The money-weighted return applies to the concept of IRR to investment portfolios. The money-weighted rate of return is defined as the internal rate of return on a portfolio, taking into account all cash inflows and outflows. The beginning value is an inflow, as are all deposits into the account. All withdrawals from the account are outflows, as is the ending value.

The time-weighted rate of return measures compound growth. It is the rate at which 1$ compounds over a specified performance horizon. Time-weighting is the process averaging a set of values over time. The annual time-weighted return for an investment may be computed by performing the following steps :

The geometrical mean return allows us to express the time-weighted return as an annual compound rate, even though we have more than one year of data. In the investment management industry, the time-weighted rate of return is the preferred method of performance measurement, because it is not affected by the timing of cash inflows and outflows.

E. Calculate and interpret the bank discount yield, holding period yield, effective annual yield, and money market yield for US T-bills and other money market instrument :

Bank discount yield (BDY) : Pure discount instruments such as U.S. T-bills are quoted differently from U.S. government bonds. T-bills are quoted on a bank discount basis, which is based on the face value of the instrument instead of the purchase price. The bank discount yield is computed using the following formula :

rBD = (D / F) * (360 / t)

where :

rBD = the annualized yield on a bank discount basis

D = the dollar discount, which is equal to the difference between the face value of the bill and the purchase price

F = the face value of the bill

t = number of days remaining until maturity

360 = bank convention of number of days in a year

The key distinction of the bank discount yield is that it expresses the dollar discount from the face value as a fraction of the face value, not the market price of the instrument. Another notable feature is that it is annualized by multiplying the discount-to-par by 360/t, where the market convention is to use a 360-day year versus a 365-day year. This type of annualized method assumes no compounding.

It is important for candidates to realize that a yield quoted on a bank discount basis is not representative of the return earned by an investor for the following reasons :

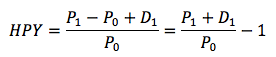

Holding period yield (HPY), or holding period return (HPR) is the total return an investor earns between the purchase date and the sale or maturity date. HPY is calculated using the following formula :

NPV decision rule : The basic idea behind NPV analysis is that if a project has a positive NPV, this amount goes to the firm’s shareholders. As such, if a firm undertakes a project with a positive NPV, shareholder wealth is increased. The NPV decision rules are summarized :

- Accept projects with a positive NPV.

- Reject projects with a negative NPV.

- When two projects are mutually exclusive (only one can be accepted), the project with the higher positive NPV should be accepted.

IRR decision rule : The following are decision rules of IRR analysis :

- Accept projects with an IRR that is greater than the firm’s required rate of return.

- Reject projects with an IRR that is less than the firm’s required rate of return.

Note that for a single project, the IRR and NPV rules lead to the same accept/reject decision.

Problems associated with the IRR method

When the acceptance or rejection of one project has no effect on the acceptance or rejection of another, the two projects are considered to be independent projects.

When only one of two projects may be accepted, the projects are considered to be mutually exclusive. For mutually exclusive projects, the NPV and IRR methods can give conflicting project rankings. Given that shareholder wealth maximization is the ultimate goal of the firm, always select the project with the greatest NPV when the IRR and NPV rules provide conflicting results.

C. Calculate and interpret a holding period return :

A holding period can be any period of time. The holding period return (HPR) is simply the percentage change in the value of an investment over the period it is held. If the asset has cash flows, such as dividend or interest payments, we refer to the return as the total return.

D. Calculate and compare the money-weighted and time-weighted rates of return of a portfolio and evaluate the performance of portfolios based on these measures :

The money-weighted return applies to the concept of IRR to investment portfolios. The money-weighted rate of return is defined as the internal rate of return on a portfolio, taking into account all cash inflows and outflows. The beginning value is an inflow, as are all deposits into the account. All withdrawals from the account are outflows, as is the ending value.

The time-weighted rate of return measures compound growth. It is the rate at which 1$ compounds over a specified performance horizon. Time-weighting is the process averaging a set of values over time. The annual time-weighted return for an investment may be computed by performing the following steps :

- Value the portfolio immediately preceding significant additions or withdrawals. Form subperiods over the evaluation period that correspond to the dates of deposit and withdrawals.

- Compute the holding period return (HPR) of the portfolio for each subperiod.

- Compute the product of (1 + HPR) for each subperiod to obtain a total return for the entire measurement period. If the total investment period is greater than one year, you must take the geometrical mean of the measurement period return to find the annual time-weighted rate of return.

The geometrical mean return allows us to express the time-weighted return as an annual compound rate, even though we have more than one year of data. In the investment management industry, the time-weighted rate of return is the preferred method of performance measurement, because it is not affected by the timing of cash inflows and outflows.

E. Calculate and interpret the bank discount yield, holding period yield, effective annual yield, and money market yield for US T-bills and other money market instrument :

Bank discount yield (BDY) : Pure discount instruments such as U.S. T-bills are quoted differently from U.S. government bonds. T-bills are quoted on a bank discount basis, which is based on the face value of the instrument instead of the purchase price. The bank discount yield is computed using the following formula :

rBD = (D / F) * (360 / t)

where :

rBD = the annualized yield on a bank discount basis

D = the dollar discount, which is equal to the difference between the face value of the bill and the purchase price

F = the face value of the bill

t = number of days remaining until maturity

360 = bank convention of number of days in a year

The key distinction of the bank discount yield is that it expresses the dollar discount from the face value as a fraction of the face value, not the market price of the instrument. Another notable feature is that it is annualized by multiplying the discount-to-par by 360/t, where the market convention is to use a 360-day year versus a 365-day year. This type of annualized method assumes no compounding.

It is important for candidates to realize that a yield quoted on a bank discount basis is not representative of the return earned by an investor for the following reasons :

- Bank discount yield annualizes using simple interest and ignores the effects of compound interest.

- Bank discount yield is based on the face value of the bond, not its purchase price.

- Bank discount yield is annualized based on a 360-day year rather than a 365-day year.

Holding period yield (HPY), or holding period return (HPR) is the total return an investor earns between the purchase date and the sale or maturity date. HPY is calculated using the following formula :

where :

P0 = initial price of the instrument

P1 = price received for instrument at maturity

D1 = interest payment (distribution)

The effective annual yield (EAY) is an annualized value, based on a 365-day year, that accounts for compound interest. It is calculated using the following equation :

The money market yield (or CD equivalent yield) is equal to the annualized holding period yield, assuming a 360-day year. Using the money market yield makes the quoted yield on a T-bill comparable to yield quotes for interest-bearing money market instruments that pay interest on a 360-day basis. The money market yield is (360/# days) * HPY.

rMM = HPY * (360 / t)

F. Convert among holding period yields, money market yields, effective annual yields, and bond equivalent yields :

Once we have established HPY, EAY, or rMM, we can use one as a basis for calculating the two others. Remember :

Basically :

P0 = initial price of the instrument

P1 = price received for instrument at maturity

D1 = interest payment (distribution)

The effective annual yield (EAY) is an annualized value, based on a 365-day year, that accounts for compound interest. It is calculated using the following equation :

The money market yield (or CD equivalent yield) is equal to the annualized holding period yield, assuming a 360-day year. Using the money market yield makes the quoted yield on a T-bill comparable to yield quotes for interest-bearing money market instruments that pay interest on a 360-day basis. The money market yield is (360/# days) * HPY.

rMM = HPY * (360 / t)

F. Convert among holding period yields, money market yields, effective annual yields, and bond equivalent yields :

Once we have established HPY, EAY, or rMM, we can use one as a basis for calculating the two others. Remember :

- The HPY is the actual return an investor will receive if the money market instrument is held until maturity.

- The EAY is the annualized HPY on the basis of a 365-day year and incorporates the effects of compounding.

- The rMM is the annualized yield that is based on price and a 360-day year and does not account for the effects of compounding.

Basically :

The bond-equivalent yield refers to 2x the semiannual discount rate. This convention stems from the yields on U.S. bonds are quoted as twice the semiannual rate, because the coupon interest is paid in two semiannual payments.

|

|